7 Strategic Asset Allocation

Associated slides: Lesson 4 — Strategic Asset Allocation

7.1 Introduction

Strategic asset allocation is a fundamental component of investment management, serving as the backbone of a long-term investment strategy. It involves setting a baseline distribution of assets across various investment categories, based on predicted rates of return for each asset class, while considering the investor’s risk tolerance and investment timeline.

7.1.1 Definition and Purpose of Strategic Asset Allocation

Strategic asset allocation refers to the process of establishing a long-term ‘base policy mix’—a proportionate combination of assets that aims to balance the risk versus return trade-off based on an investor’s specific objectives and constraints. The core purpose of this approach is to optimize the potential return for a given level of risk by carefully selecting the proportion of various asset classes such as stocks, bonds, real estate, and alternatives.

- Foundational Strategy: Unlike tactical asset allocation, which seeks to take advantage of short-term market movements, strategic asset allocation provides a foundation for building a portfolio that can weather market fluctuations and adhere to a predetermined investment approach.

7.1.2 Importance of Aligning Strategic Asset Allocation with Long-Term Investment Objectives and Risk Tolerance

- Meeting Investment Objectives: Strategic asset allocation is crucial for ensuring that investment decisions are aligned with the investor’s long-term goals, whether these goals are growth, income, or preservation of capital. By defining how assets should be distributed across different categories, investors can aim to achieve their financial targets within their expected time horizon.

- Risk Management: Effective asset allocation inherently involves managing risk by diversifying investments across a variety of asset classes. This diversification helps reduce the risk of significant losses by spreading exposure across assets that have varying reactions to the same economic events.

- Consistency and Discipline: A well-defined strategic asset allocation strategy helps investors maintain a disciplined approach in their investing practices. It reduces the risk of making impulsive decisions based on short-term market trends and focuses on broader financial goals.

- Adaptability to Changing Financial Goals and Risk Profiles: Over time, an investor’s financial situation, goals, and risk tolerance may evolve due to changes in personal life, economic conditions, or market environments. Regular reviews and adjustments of the asset allocation ensure that the portfolio continues to meet the investor’s needs.

7.1.3 Conclusion

Strategic asset allocation is not just about choosing the right mix of assets; it’s about creating a robust framework that guides investment decisions over the long term. By aligning asset allocation with an individual’s financial goals and risk tolerance, investors can forge a path toward achieving their financial aspirations with confidence. This chapter will explore the intricate details and methodologies behind strategic asset allocation, providing investors and financial advisors with the insights needed to construct effective and resilient investment portfolios.

Strategic asset allocation is a core component of the CFA curriculum’s Portfolio Management topic. The CFA program emphasizes the importance of aligning asset allocation with an investor’s risk tolerance and investment horizon to optimize portfolio performance. It teaches candidates about the critical role of diversification in reducing risk while potentially enhancing returns. Understanding these principles is essential for CFA candidates aiming to develop robust investment strategies that are responsive to client needs and market conditions.

7.2 Establishing Investment Guidelines

7.2.1 Developing Investment Guidelines

Investment guidelines serve as the operational framework for managing a client’s portfolio, ensuring that all investment decisions are aligned with the client’s specific financial objectives, risk tolerance, and investment horizon. These guidelines are crucial for maintaining discipline in the investment process, providing clear instructions for how to manage the portfolio under normal market conditions and when adjustments are needed.

- Incorporation of Client’s Financial Goals:

- Investment guidelines begin with a thorough understanding of the client’s financial aspirations, such as retirement savings, purchasing a home, funding education, or building an emergency fund.

- Specific goals should be quantified where possible (e.g., “accumulate $500,000 for retirement by 2040”) and prioritized to help determine the appropriate asset allocation and risk level.

- Consideration of Risk Tolerance:

- The guidelines must reflect the client’s risk tolerance, which influences the asset mix and the selection of individual investments.

- This involves an assessment of how much volatility the client is willing to accept, and their capacity to endure potential financial losses, especially in adverse market conditions.

- Accounting for Investment Horizon:

- The client’s investment horizon, or the time frame they have to achieve their financial goals, is a critical factor in setting investment guidelines.

- Longer horizons typically allow for a higher allocation to riskier assets like equities, which may fluctuate more in the short term but tend to offer higher returns over the long term.

7.2.2 Constructing a Strategic Asset Allocation Model

A strategic asset allocation model acts as a blueprint for building and maintaining a client’s portfolio. It specifies how assets should be allocated across various asset classes to optimize the potential for return while managing risk appropriately.

- Defining Asset Classes:

- Determine which asset classes will be included in the portfolio, such as equities, bonds, real estate, commodities, and alternatives.

- Each asset class should be chosen based on its expected role in achieving the portfolio’s goals and its behavior under different market conditions.

- Setting Allocation Percentages:

- Establish the target allocation percentages for each asset class based on the client’s risk tolerance and investment horizon.

- These percentages are designed to balance the growth potential with risk mitigation, aiming to maximize returns while keeping risk within acceptable limits.

- Rebalancing Criteria:

- Define clear criteria for when and how the portfolio should be rebalanced to its target allocations. This could involve setting thresholds for deviation from the original allocations (e.g., rebalance when any asset class deviates by more than 5% from its target).

- Rebalancing ensures that the portfolio remains aligned with the client’s strategic asset allocation over time, even as market movements may cause shifts in the actual asset mix.

7.2.3 Conclusion

Developing robust investment guidelines and constructing a strategic asset allocation model are critical steps in ensuring that investment management aligns with the client’s long-term objectives. These frameworks not only guide day-to-day decision-making but also provide a structured approach to handling market volatility and adjusting to changes in the client’s life circumstances or financial goals. By adhering to these guidelines, financial advisors can help clients navigate through the complexities of investing and achieve their financial aspirations with confidence.

When developing investment guidelines, always ensure they are clear, measurable, and easily understandable by all stakeholders. Use templates to standardize the investment guideline process across portfolios but customize them to fit specific client needs. Regularly review these guidelines in consultation with clients to ensure they remain aligned with their evolving financial goals and market conditions.

7.3 Defining Asset Classes for Allocation

Asset allocation is a critical element of strategic investment planning, involving the distribution of investment funds across various asset classes. Each class offers distinct risk and return characteristics, and plays a unique role in portfolio diversification. Understanding these differences is key to constructing a balanced portfolio that meets specific financial goals and risk tolerance.

7.3.1 Traditional Asset Classes

- Stocks (Equities):

- Description: Stocks represent ownership in a company. Investors who buy stocks expect to earn returns from dividends and capital appreciation.

- Role in Portfolio: Stocks are typically associated with higher potential returns compared to other asset classes, but also higher volatility and risk. They play a crucial role in growth-oriented portfolios.

- Correlation: Generally, stocks have a low correlation with bonds and certain alternative assets, making them a good tool for diversification.

- Bonds (Fixed-Income Securities):

- Description: Bonds are debt instruments issued by corporations or governments. Investors receive regular interest payments, and the principal amount is returned at maturity.

- Role in Portfolio: Bonds are considered lower risk compared to stocks, often providing steady income with less volatility. They are crucial for income generation and capital preservation.

- Correlation: Bonds often move inversely to stocks, especially government bonds, which can increase in value during stock market downturns due to their perceived safety.

- Cash and Cash Equivalents:

- Description: This class includes highly liquid securities with short maturities, such as treasury bills, money market funds, and certificates of deposit.

- Role in Portfolio: Cash provides stability and quick access to funds without risking capital. It is essential for liquidity needs and safety in a portfolio.

- Correlation: Cash has a very low or negative correlation with other asset classes, offering an excellent buffer during market turbulence.

7.3.2 Alternative Asset Classes

- Real Estate:

- Description: Real estate investment can be direct (purchasing property) or indirect (REITs - Real Estate Investment Trusts). It includes both residential and commercial properties.

- Role in Portfolio: Real estate typically offers appreciation in value, rental income, and diversification benefits. It can act as a hedge against inflation since property values and rents tend to rise with inflation.

- Correlation: Real estate often has a low correlation with stocks and bonds, providing diversification benefits.

- Commodities:

- Description: Commodities include physical goods like oil, gold, and agricultural products. Investments can be made directly in physical commodities or through futures contracts and commodity-focused funds.

- Role in Portfolio: Commodities can protect against inflation and provide diversification. Prices often move based on different factors than financial securities, such as weather or geopolitical tensions.

- Correlation: Typically, commodities exhibit a different return pattern compared to traditional securities, offering strong diversification benefits in a multi-asset portfolio.

- Private Equity:

- Description: Private equity involves investing in companies that are not publicly traded on a stock exchange. This includes venture capital, buyouts, and private investment in public equity (PIPE).

- Role in Portfolio: Private equity aims for higher returns than public markets can potentially provide, though with higher risk and liquidity constraints.

- Correlation: Due to the long investment horizons and capital commitment, private equity may show lower correlation with public equities and bonds, enhancing portfolio diversification.

7.3.3 Conclusion

Understanding the characteristics, roles, and correlations of various asset classes is fundamental to effective strategic asset allocation. By appropriately combining traditional and alternative asset classes, investors can achieve a diversified portfolio that balances the potential for higher returns with risk management, aligning with their long-term financial objectives and risk tolerance.

7.4 Geographic Diversification

Geographic diversification is an essential strategy within portfolio management, aimed at spreading investment risk and opportunity across various global markets. This approach can protect against local or regional economic downturns and capitalize on growth in different parts of the world.

7.4.1 Rationale for Country-Specific Investments

- Access to Unique Opportunities: Investing in specific countries can provide access to unique economic sectors or industries that are not as prevalent or developed in the investor’s home market. For instance, investing in a country with a booming technology sector or a growing renewable energy market.

- Benefit from Economic Growth: Country-specific investments allow investors to benefit directly from the economic growth of a particular region. Fast-growing economies, often found in emerging markets, can offer higher returns, although with higher risk.

- Hedge Against Local Market Volatility: By diversifying geographically, investors can reduce the impact of volatility in their local markets. If one market performs poorly, losses can potentially be offset by gains in another.

7.4.2 Benefits of International Diversification

- Reduced Portfolio Risk: International diversification spreads investment risk across a broader economic base, reducing the impact of country-specific shocks such as political instability, economic recessions, or currency fluctuations.

- Enhanced Return Potential: Global markets do not always move in tandem; thus, international diversification can capitalize on growth in different regions, potentially enhancing overall portfolio returns.

- Exposure to Foreign Currencies: Investing internationally involves exposure to foreign currencies, which can provide an additional layer of diversification and an opportunity to profit from currency movements.

7.4.3 Considerations for Emerging Markets vs. Developed Markets

- Risk and Growth Potential: * Emerging Markets: Typically offer higher growth potential due to rapid economic development, urbanization, and population growth. However, these markets also carry higher risks, including political instability, less mature financial markets, and greater volatility.

- Developed Markets: Generally provide more stability, well-established market structures, and lower volatility. While the growth rates in developed markets might be lower, these markets often offer safer investment environments and more predictable returns.

- Regulatory and Operational Considerations: Investors must consider the regulatory environment, market liquidity, and the ease of doing business in each country. Emerging markets might have less stringent regulations and greater bureaucratic challenges, which can increase operational risks.

- Economic and Political Climate: The economic policies, government stability, and geopolitical situation of a country significantly impact its market’s risk and return profiles. These factors must be carefully evaluated when considering investments in both emerging and developed markets.

7.4.4 Conclusion

Geographic diversification is a sophisticated strategy that requires an understanding of global economic dynamics, local market conditions, and specific regional risks and opportunities. By effectively allocating assets across various geographic regions, investors can mitigate risks associated with any single country while potentially enhancing portfolio performance. This strategy is crucial for those seeking to build resilient, well-rounded investment portfolios capable of navigating the complexities of the global economy.

Utilize country-specific ETFs and mutual funds to achieve geographic diversification without the need for in-depth knowledge of foreign markets. These instruments provide an effective way to gain exposure while mitigating individual stock risk. Also, consider using currency-hedged ETFs to reduce the impact of foreign exchange volatility on your international investments.

7.5 Currency Allocation

Currency allocation is a critical aspect of international investing. As investors diversify their portfolios globally, they must also consider the impact of currency exposure on their investments. Currency movements can significantly affect the overall returns of international assets, making it essential to understand and manage currency risks.

7.5.1 Impact of Currency Exposure on International Investments

- Influence on Returns: Currency fluctuations can either enhance or erode the returns from international investments. For example, if an investor holds stocks in a country whose currency appreciates against their home currency, the returns could be magnified when converted back to the home currency. Conversely, a depreciating currency can diminish returns.

- Portfolio Volatility: Currency variations can add an extra layer of volatility to a portfolio. Exchange rates are influenced by numerous factors including economic indicators, central bank policies, political stability, and market sentiment. This volatility can be especially pronounced in regions with unstable economic conditions.

7.5.2 Strategies for Currency Diversification and Managing Currency Risk

- Currency Hedging:

- Hedging Instruments: Investors can use financial instruments such as futures, options, and forwards to hedge against currency risk. These instruments can be structured to offset potential losses caused by adverse currency movements.

- Hedging Strategies: Deciding whether to hedge currency exposure depends on the investor’s risk tolerance, investment horizon, and the cost of hedging. Some investors may choose to hedge significant exposures in highly volatile currencies while accepting the currency risk in more stable or strategically important regions.

- Currency Diversification:

- Multiple Currency Exposure: Just as diversifying investments across different asset classes and geographies can reduce risk, holding assets in a variety of currencies can also buffer against currency volatility. By spreading currency exposure, investors can potentially mitigate the risk of any single currency’s adverse movement significantly impacting their portfolio.

- Balanced Currency Portfolio: Creating a balanced portfolio that includes a mix of currencies from developed and emerging markets can provide both stability and growth potential. Developed market currencies often offer stability, while emerging market currencies can offer growth opportunities, albeit with higher risk.

- Natural Currency Hedging:

- Revenue Matching: Investors can engage in natural hedging by matching foreign currency revenues with costs incurred in the same currency. For example, if an investor owns a business or assets that incur expenses in a foreign currency, holding investments that generate revenue in the same currency can naturally offset currency fluctuations.

- Asset Location: Choosing investment locations can also serve as a natural hedge. Investing in markets that are likely to appreciate against the investor’s home currency can strategically position the portfolio to benefit from these movements.

7.5.3 Conclusion

Managing currency risk is an indispensable part of international investing. Effective currency allocation strategies, including hedging, diversification, and natural hedging methods, can help investors minimize unwanted currency exposure and enhance the risk-return profile of their portfolios. By carefully considering the impact of currency movements and employing strategies to manage these risks, investors can achieve more stable and potentially higher returns on their international investments.

For practical currency risk management, start by identifying your natural currency exposures and consider matching these with corresponding assets or liabilities. Utilize currency forward contracts to hedge against unwanted exposure. Always monitor exchange rate forecasts and adjust your hedging strategies accordingly to align with anticipated market trends.

7.6 Deciding on the Asset Mix

Determining the appropriate asset mix is a pivotal task in strategic asset allocation. This process involves selecting the right combination of asset classes to meet specific investment objectives while managing risk effectively. The asset mix not only influences the potential returns and risk profile of a portfolio but also reflects the investor’s financial situation, risk tolerance, and market expectations.

7.6.1 Methods for Determining the Appropriate Mix of Asset Classes

- Historical Performance Analysis:

- Role of Historical Data: Historical performance data of various asset classes provide insights into their risk and return profiles over different market conditions. This analysis helps in understanding how each asset class has reacted to economic cycles, interest rate changes, and geopolitical events.

- Application: By analyzing trends and volatility from historical data, investors can gauge which asset classes are likely to perform well under current or expected economic conditions, and how they contribute to the overall portfolio volatility.

- Future Outlooks:

- Economic and Market Forecasts: Consideration of future market outlooks involves evaluating economic forecasts, including GDP growth, inflation rates, and monetary policy changes, which can impact asset classes differently.

- Impact on Asset Classes: For example, a forecasted rise in interest rates may negatively impact bond prices, suggesting a reduced allocation to fixed income in favor of asset classes less sensitive to interest rate changes, like equities or real estate.

- Client-Specific Factors:

- Risk Tolerance and Time Horizon: The asset mix must align with the client’s risk tolerance and investment horizon. Clients with higher risk tolerance and longer time horizons may be more suited for a higher allocation to equities, while more conservative investors or those nearing retirement might prefer bonds or cash.

- Financial Goals: Specific financial goals can dictate adjustments in the asset mix. For instance, funding a child’s education within a decade may require maintaining a certain percentage of the portfolio in less volatile assets as the goal approaches.

7.6.2 Utilizing Optimization Models to Derive the Asset Mix

- Mean-Variance Optimization (MVO):

- Description: MVO is a quantitative tool used to calculate the best possible asset allocation that maximizes returns for a given level of risk. This model uses the expected returns, standard deviations, and correlations of the asset classes to generate an efficient frontier of optimal portfolios.

- Application: By plotting various potential portfolios on the efficient frontier, investors can select a portfolio that offers the highest expected return for a specific level of risk.

- Monte Carlo Simulations:

- Description: This method uses computer algorithms to simulate thousands of possible scenarios for different asset mixes, allowing investors to see a range of outcomes based on a combination of historical data and projected economic conditions.

- Application: Monte Carlo simulations help in understanding the potential range of outcomes and the likelihood of achieving specific investment targets, thus aiding in making informed decisions about the asset mix.

- Constraint-Based Optimization:

- Incorporating Constraints: Real-world portfolios often face various constraints such as liquidity requirements, legal restrictions, and specific client mandates. Constraint-based optimization models incorporate these limitations to refine the asset allocation process.

- Balancing Needs and Constraints: These models help balance the theoretical ideal portfolio with practical considerations, ensuring the asset mix is both optimized and feasible under actual investing conditions.

Leverage software tools like portfolio management systems that support mean-variance optimization and Monte Carlo simulations to streamline the process of deciding on asset mixes. Consider the use of sensitivity analysis to understand how different input assumptions affect your asset allocation outcomes, thereby enhancing decision-making confidence.

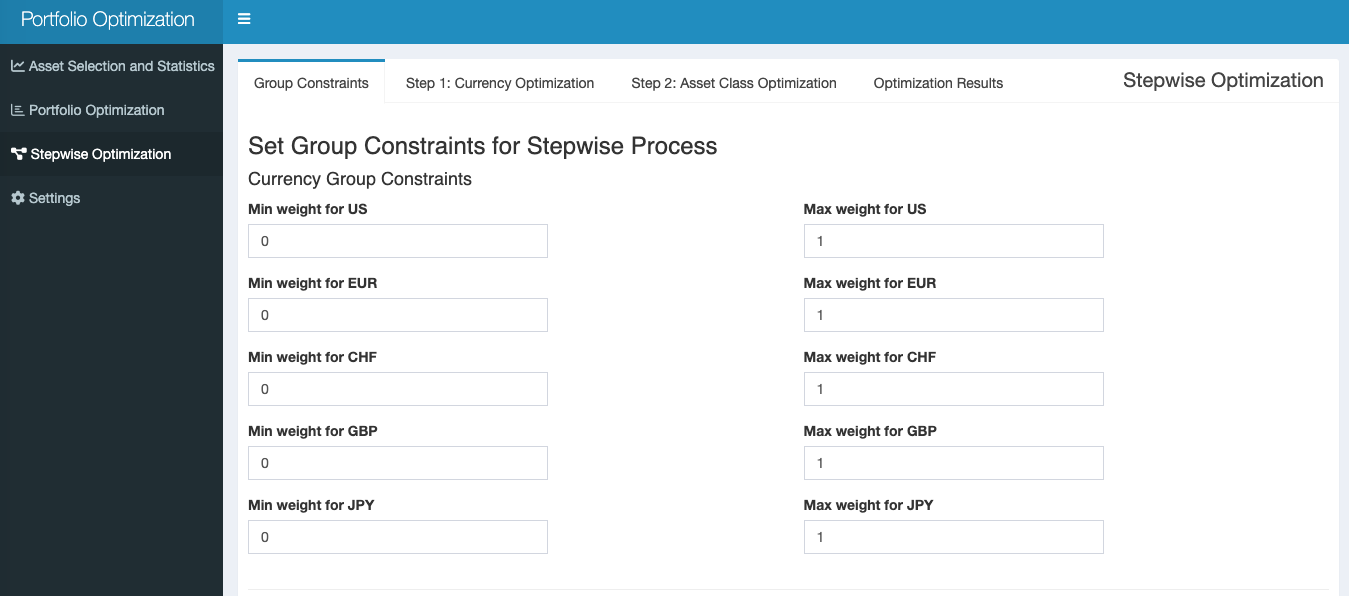

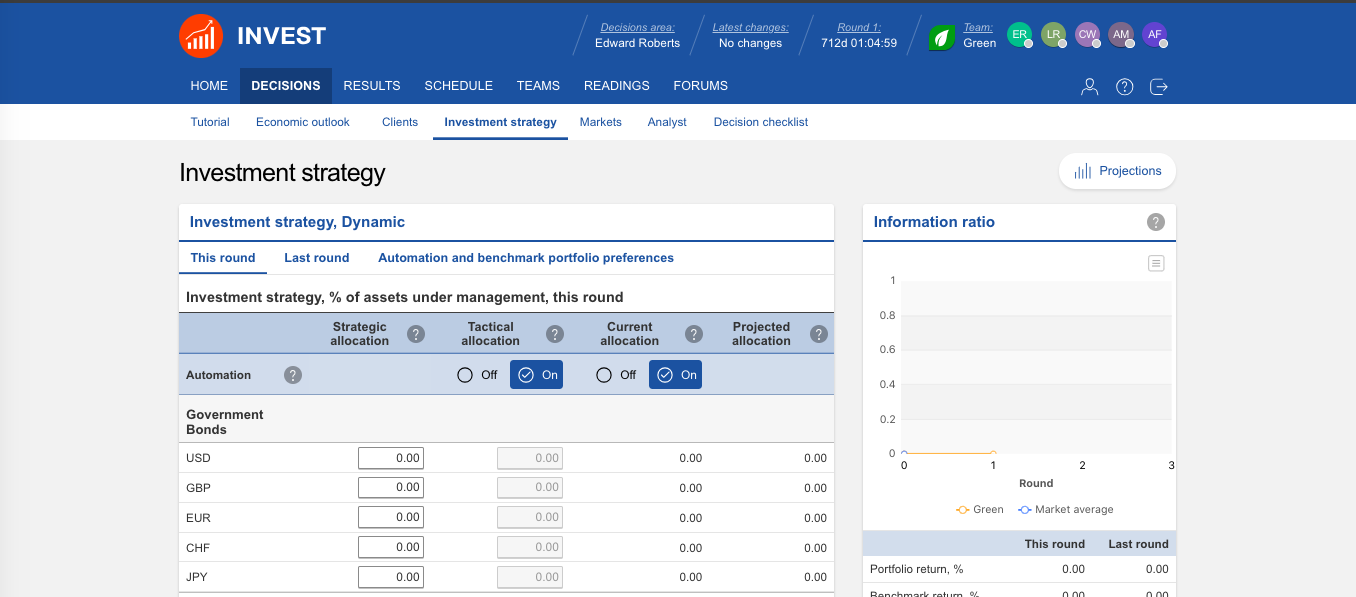

7.7 Strategic Asset Allocation in Cesim Invest

Similarly to strategic financial analysis, the strategic asset allocation in Cesim Invest can be performed in the app that is available under the link below: https://inno.uni.li/apps/invest/.

Under Stepwise Optimisation/Group Constraints Currency and Asset Class Group Constraints can be specified based on the outcomes of client and strategic financial analyses.

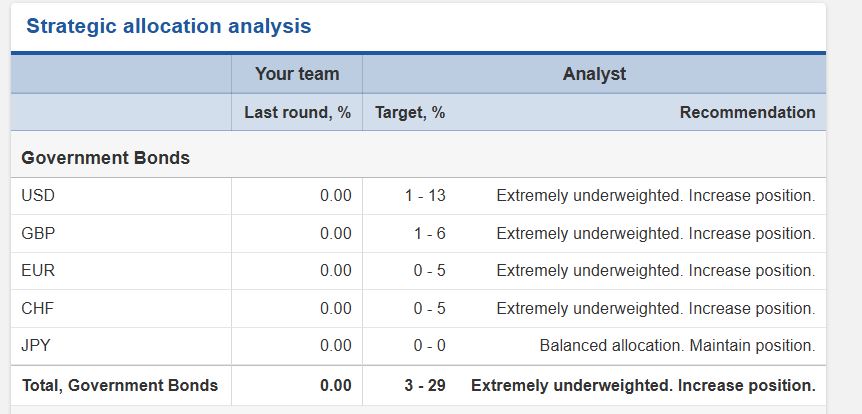

As a starting point one could use the recommendation available under Decisions/Analyst.

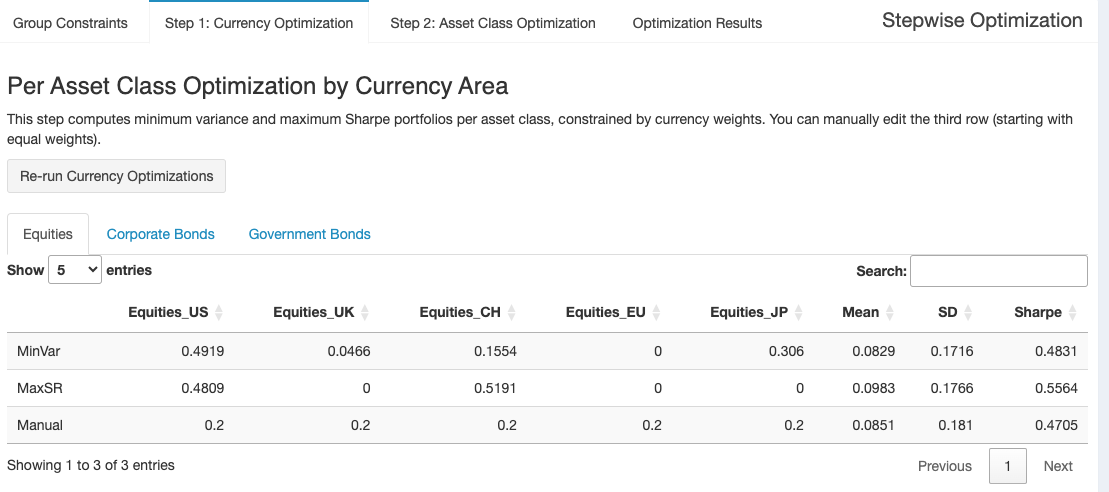

Portfolio optimisation based on defined constraints is performed in two steps. At the currency optimisation step minimum variance and maximum Sharpe portfolios per asset class (equities, corporate bonds, government bonds), constrained by currency weights, become available.

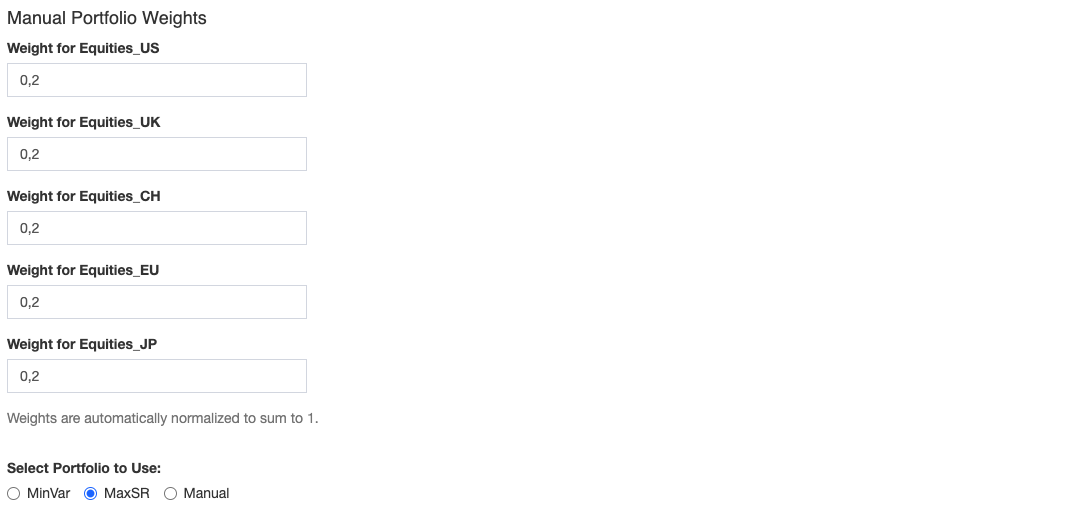

There is also an option to create a portfolio with manually edited weights, such as equal ones.

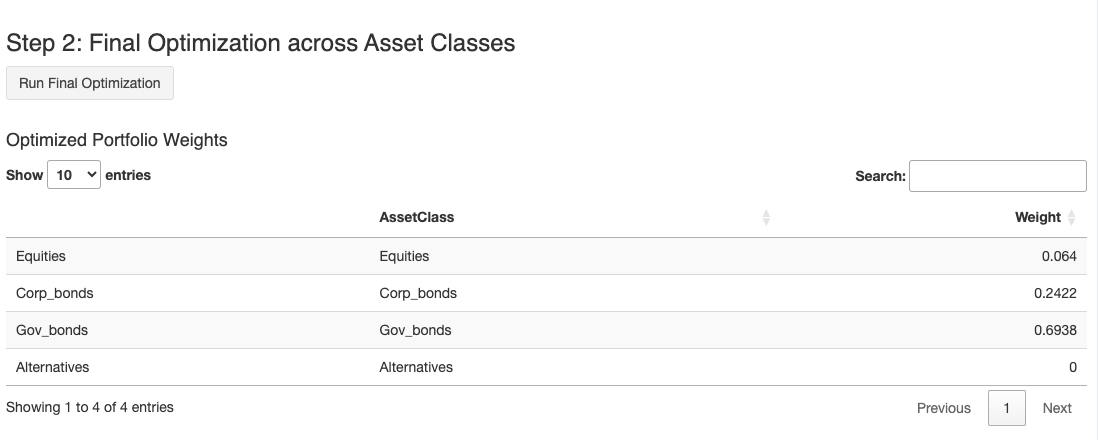

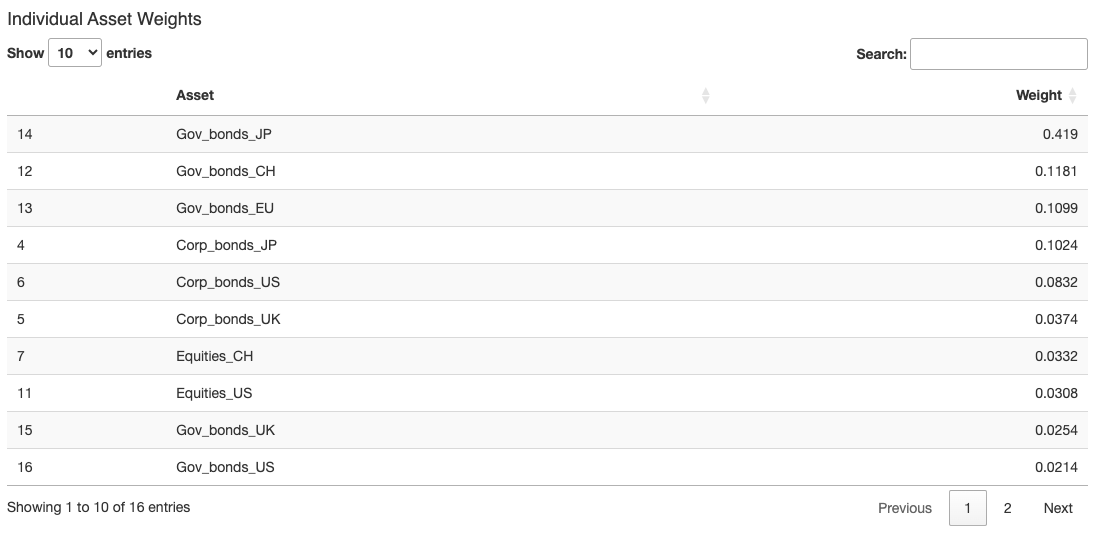

One of these portfolios (Minimum Variance, Maximum Sharpe Ratio or Manual), based on the client profile, should be selected for the final step of the portfolio optimisation. For example, selecting MaxSR with the constraints set to a minimum of 0 and a maximum of 1 for each as above, will result in the following output below.

One of these portfolios (Minimum Variance, Maximum Sharpe Ratio or Manual), based on the client profile, should be selected for the final step of the portfolio optimisation. For example, selecting MaxSR with the constraints set to a minimum of 0 and a maximum of 1 for each as above, will result in the following output below.

The above individual asset weights serve as input for Strategic Allocation available under Decisions/Investment strategy in Cesim Invest.

The above individual asset weights serve as input for Strategic Allocation available under Decisions/Investment strategy in Cesim Invest.

7.7.1 Conclusion

Deciding on the appropriate asset mix is a nuanced process that requires balancing historical data, future projections, and individual investor needs with sophisticated optimization models. By meticulously applying these methods, investors can craft a portfolio that not only aims for optimal financial returns but also aligns closely with personal or institutional investment goals, ensuring a strategic approach to asset allocation.

When defining your asset mix, consider using interactive tools like asset allocation calculators to visualize the potential impact of different asset class combinations on your portfolio’s risk and return profiles. Additionally, regularly update your market research to keep abreast of how shifts in economic indicators could impact asset classes differently, ensuring your mix remains optimized for current conditions.

7.8 Incorporating Sustainability and Global Trends

In today’s investment landscape, sustainability and global economic trends significantly influence strategic asset allocation decisions. As awareness of environmental, social, and governance (ESG) factors grows, investors are increasingly considering how these elements can affect long-term investment returns and risk profiles. This subchapter explores the integration of sustainability and global trends into asset allocation strategies, focusing on the inclusion of green investments and the drive towards a low-carbon economy.

7.8.1 Influence of Global Economic Trends and Sustainability on Asset Allocation

- Impact of Global Trends:

- Economic Shifts: Changes in global economic dynamics, such as the rise of emerging markets, technological advancements, and demographic shifts, can alter the investment landscape. These trends may affect various asset classes differently, necessitating adjustments in asset allocation to capitalize on growth opportunities or mitigate risks.

- Regulatory Changes: Increasingly stringent regulations on carbon emissions and corporate governance worldwide impact industries and asset classes. For instance, carbon-heavy sectors may face higher costs and regulatory risks, making them less attractive to sustainability-conscious investors.

- Sustainability Factors:

- Environmental Concerns: As the effects of climate change become more pronounced, there is a growing emphasis on investments that support environmental sustainability. This includes sectors like renewable energy, sustainable agriculture, and green technology.

- Social and Governance Issues: Social trends, including concerns about social inequality and corporate governance practices, are pushing investors to consider the societal impact of their investments. This shift can influence the attractiveness of certain companies or sectors based on their ESG performance.

7.8.2 Adapting Allocation to Incorporate Green Investments

- Green Investments:

- Renewable Energy Assets: Including assets like solar and wind power facilities in the portfolio not only supports sustainability goals but also positions the portfolio to benefit from the growth potential in these sectors.

- Green Bonds: Investing in green bonds, which are specifically used to fund projects that have positive environmental and/or climate benefits, offers a way to contribute to environmental sustainability while receiving steady income.

- Incorporating Low-Carbon Economy Assets:

- Low-Carbon Index Funds: These funds focus on companies that generate lower carbon emissions and are better positioned to thrive in a low-carbon economy. Such funds can be a strategic component of the asset mix, reducing the portfolio’s carbon footprint and aligning with global carbon reduction goals.

- Sustainable Real Estate and Infrastructure: Investments in green buildings and sustainable infrastructure projects that use energy-efficient materials and technologies can offer long-term benefits both financially and environmentally.

7.8.3 Strategies for Integrating Sustainability into Asset Allocation

- ESG Integration:

- Comprehensive ESG Evaluation: Systematically incorporate ESG criteria into the investment analysis process. This includes evaluating potential investments based on their ESG scores, which reflect their adherence to sustainable practices.

- Stakeholder Engagement: Actively engage with companies to encourage them to improve their sustainability practices, which can enhance long-term returns and reduce investment risks.

- Thematic Investing:

- Focus on Sustainability Themes: Allocate assets to investment opportunities that are likely to benefit from sustainability trends, such as water management, clean energy, and sustainable consumer products.

7.8.4 Conclusion

Incorporating sustainability and adapting to global economic trends are increasingly important in strategic asset allocation. By aligning investment strategies with these factors, investors can not only enhance potential financial returns and manage risks more effectively but also contribute to broader societal goals. This approach requires a dynamic and forward-looking investment strategy that remains responsive to both emerging opportunities and evolving risks in the global marketplace.

The CFA curriculum increasingly recognizes the significance of ESG factors in investment decision-making, aligning with global trends towards sustainable investing. Ethical and professional standards within the curriculum encourage CFA candidates to consider environmental, social, and governance factors as integral components of comprehensive investment analysis. This approach not only aligns with ethical investing practices but also caters to a growing demand within the financial industry to deploy capital in sustainability-focused initiatives.

7.9 Revisiting and Adjusting the Allocation

7.9.1 Portfolio Rebalancing

Strategic asset allocation is not a set-it-and-forget-it strategy. It requires continuous monitoring and periodic adjustments to ensure that the investment portfolio remains aligned with the client’s financial goals, risk tolerance, and time horizon. This subchapter discusses the processes of ongoing monitoring, rebalancing, and adjusting asset allocations in response to significant market changes or personal life events.

7.9.2 Ongoing Monitoring and Rebalancing Procedures

- Monitoring the Portfolio:

- Performance Tracking: Regularly assess the performance of each asset class within the portfolio against its benchmarks and the overall investment objectives. This helps identify any deviations that may require corrective actions.

- Market Condition Observations: Keep abreast of economic and market developments that could impact the investment landscape. This includes tracking interest rate movements, economic indicators, and geopolitical events that could influence asset performances.

- Rebalancing Strategies:

- Scheduled Rebalancing: Implement a rebalancing schedule (e.g., quarterly, biannually) to adjust the portfolio’s asset allocation to its target mix. This systematic approach helps in maintaining the desired level of risk and return characteristics over time.

- Threshold-based Rebalancing: Set specific thresholds for rebalancing, such as when an asset class’s actual allocation deviates by more than a predetermined percentage (e.g., 5%) from its target allocation. This strategy ensures that the portfolio does not drift too far from its strategic asset allocation, minimizing risk and optimizing returns.

7.9.3 Adjusting the Strategic Asset Allocation

- Response to Market Changes:

- Short-term Adjustments: In the face of significant market volatility, consider tactical adjustments to the asset allocation to protect the portfolio from losses or to capitalize on temporary market opportunities. However, these adjustments should always align with the long-term strategic objectives of the portfolio.

- Long-term Adjustments: Larger shifts in the economic environment, such as a recession or a booming market, might necessitate more substantial changes to the asset allocation to optimize the portfolio for the new conditions.

- Adapting to Life Events:

- Personal Milestones: Significant life events such as marriage, the birth of a child, approaching retirement, or receiving a large inheritance may alter a client’s financial situation, goals, or risk tolerance. Such events require a review and potential adjustment of the asset allocation to reflect the new circumstances.

- Financial Changes: Changes in the client’s financial status, such as a career change, buying a home, or significant changes in income levels, can also impact their investment objectives and need to be considered in the asset allocation strategy.

7.9.4 Best Practices for Revisiting and Adjusting the Allocation

- Use of Technology: Utilize financial technology tools to aid in monitoring market trends and portfolio performance, providing timely data that supports informed decision-making.

- Client Communication: Maintain open lines of communication with clients to ensure that any changes in their life circumstances or financial goals are promptly reflected in their investment strategy.

- Professional Guidance: Regular consultations with financial advisors or investment professionals can provide expert insights and recommendations for adjusting asset allocations in line with evolving market conditions and personal needs.

7.9.5 Conclusion

Effective asset allocation requires a dynamic approach that considers continuous monitoring, regular rebalancing, and timely adjustments. By establishing robust procedures for revisiting and adjusting the portfolio, investors can ensure that their investment strategy remains responsive to both market dynamics and personal circumstances, thereby optimizing the potential for achieving their long-term financial objectives.

According to the CFA curriculum, effective asset allocation requires not only initial strategic planning but also ongoing adjustments based on systematic market analysis and emerging risks. The curriculum covers quantitative methods, including Monte Carlo simulations, that help in understanding and managing portfolio risks through dynamic modeling. Furthermore, the CFA standards advocate for periodic portfolio reviews and rebalancing, ensuring that asset allocations continue to reflect the investor’s objectives and market realities, thereby maintaining the relevance and effectiveness of the investment strategy.

Set automated alerts to notify you when portfolio allocations deviate from target thresholds to prompt timely rebalancing. Use decision matrices to outline specific actions under various market scenarios, simplifying the adjustment process. Engage in bi-annual strategy sessions with clients to discuss and potentially revise asset allocations based on new financial data or changes in life circumstances.

7.10 Conclusion: The Essential Role of Strategic Asset Allocation

7.10.1 Summarizing the Importance of Strategic Asset Allocation

Strategic asset allocation stands as a cornerstone of effective investment management, crucial for navigating the complexities of the financial markets and achieving long-term investment success. This disciplined approach involves distributing investments across a carefully selected mix of asset classes to optimize the balance between risk and return. It is designed to align closely with an investor’s financial goals, risk tolerance, and investment horizon, providing a structured framework that guides the portfolio construction process.

The critical role of strategic asset allocation lies in its ability to enhance portfolio performance through diversification. By spreading investments across different asset classes, geographical regions, and sectors, strategic asset allocation helps mitigate risks associated with market volatility and economic downturns. It leverages the strengths of various asset types, taking advantage of their unique characteristics and performance patterns, which can lead to more stable and potentially higher returns over the long term.

7.10.2 Reinforcing the Need for Flexibility and Adaptation

While strategic asset allocation provides a blueprint for building a portfolio, it is important to recognize that it should not be a static strategy. The financial markets are dynamic, influenced by a myriad of factors including economic shifts, geopolitical events, and technological advancements. These changes can alter the risk-return profile of different asset classes, necessitating periodic reviews and adjustments to the asset allocation.

Regular monitoring of the portfolio and the broader market conditions is essential. This ongoing oversight ensures that the asset allocation continues to meet the investor’s objectives and adapts to any changes in their personal circumstances, financial goals, or risk tolerance. Scheduled rebalancing helps in realigning the portfolio to its target asset allocation, correcting any deviations that may occur due to market movements.

Moreover, life events such as retirement, changes in income, or shifts in financial goals also require adjustments to the asset allocation. Such personal changes can impact an investor’s capacity to bear risk or alter their financial needs, making it imperative to modify the asset allocation to reflect the new reality.

7.10.3 Final Conclusion

Strategic asset allocation is not merely a set of investment guidelines but a fundamental strategy that requires commitment, discipline, and responsiveness. It plays a pivotal role in the pursuit of investment success, helping investors navigate through market uncertainties and achieve their long-term financial objectives. By embracing flexibility and adapting to both market and personal changes, investors can maintain a relevant and effective investment strategy that supports their evolving needs and aspirations. This approach underscores the importance of asset allocation not just as a foundation for investment decisions but as a dynamic and integral part of ongoing financial management.