4 Client Analysis

Associated slides: Lesson 3 — Client Discovery & the Investment Policy Statement

4.1 Introduction

In investment management, understanding each client’s specific needs, goals, and risk tolerance is essential for crafting a tailored investment strategy aligned with their financial objectives. This understanding forms the backbone of client analysis, a foundational step in ensuring that investment decisions genuinely reflect client circumstances and aspirations. Client analysis involves gathering, verifying, and documenting essential client data through the Know Your Client (KYC) process, ultimately supporting an ethical and customized approach to investment.

4.1.1 Importance of Thorough Client Analysis

Thorough client analysis is essential for ensuring that the financial advice and products offered match the client’s investment profile. This process involves assessing the client’s financial situation, investment experience, risk tolerance, and long-term goals. A deep understanding of these factors allows financial advisors to recommend investments that are suitable and sustainable, thereby enhancing client satisfaction and retention. For wealth managers and advisors, effective client analysis leads to better-informed decisions, optimized investment performance, and minimized risks associated with mismatched investment advice.

4.1.2 Understanding the KYC Principle

The KYC principle is a regulatory requirement for financial services providers to verify the identity, suitability, and risks involved with maintaining a business relationship. The process includes gathering personal information such as name, age, address, income, and investment experience. This information is crucial not only for identity verification but also for assessing the potential for illegal activities such as money laundering or terrorist financing. Moreover, KYC practices enable advisors to understand the client’s financial needs and investment objectives thoroughly, which is crucial for providing personalized advice.

4.1.3 Regulatory Aspects of KYC

KYC regulations are part of broader anti-money laundering (AML) laws that govern the financial industry globally. Compliance with these regulations requires institutions to perform due diligence to ensure that clients are properly assessed before establishing a financial relationship. The KYC process involves several key components:

- Client Identification Program (CIP): Verifying the identity of individuals wishing to conduct financial transactions.

- Customer Due Diligence (CDD): Assessing the risk profile of the client and monitoring their transactions.

- Enhanced Due Diligence (EDD): For higher-risk customers, a more thorough check is conducted, which may include detailed financial and background checks.

In line with the CFA curriculum, understanding the KYC principle is fundamental for investment professionals. The CFA Institute emphasizes ethical and professional standards, of which client analysis is a crucial part. The curriculum covers the importance of understanding client circumstances and constructing investment solutions that consider clients’ financial constraints, risk objectives, and personal circumstances. Incorporating KYC and client analysis principles into investment decisions ensures that advisors adhere to both ethical standards and regulatory requirements, providing a foundation for trust and integrity in the client-advisor relationship.

4.1.4 Conclusion

Client analysis, underpinned by the KYC principle, is integral to the successful management of client portfolios. It ensures that investment strategies are not only compliant with regulatory standards but also precisely tailored to meet the diverse needs of clients. As financial markets evolve and client needs become more complex, the role of comprehensive client analysis will continue to grow in importance, shaping the future of personalized financial advice and investment management.

In our game we will deal with various different client types. here are two examples for such clients:

1. Conservative Swiss Client

This type of client is typically focused on capital preservation and generating moderate returns without taking on unnecessary risks. Being in her 50s, this client may be approaching retirement or at a stage in life where financial security and income stability are prioritized. As a resident of Switzerland, she is likely accustomed to stability and may value investments that reflect this mindset, such as Swiss government bonds or other low-risk, highly-rated instruments. With no specific focus on ESG, her portfolio doesn’t need to integrate sustainability criteria.

Example Client Descriptions:

- Sabine Meyer

- Age: 54

- Location: Zurich, Switzerland

- Occupation: Senior Manager in a Swiss private bank

- Family: Married with two adult children

- Financial Goals: Wealth preservation and conservative growth over the next 10-15 years, ensuring stability during retirement.

- Claudia Fischer

- Age: 52

- Location: Geneva, Switzerland

- Occupation: Consultant for multinational corporations

- Family: Recently widowed, with one adult child pursuing further education

- Financial Goals: Secure income generation, long-term capital preservation, financial support for her child’s education, and stability in her retirement years.

2. Dynamic US ESG Client

This client type is younger, highly motivated by growth, and open to taking on more risk for potentially higher returns. Hailing from Silicon Valley, he may have a strong interest in technology and innovation. While his primary focus is on returns, he is also keen to include sustainability metrics - provided they do not compromise profitability.

Example Client Descriptions:

- Michael Chen

- Age: 28

- Location: Palo Alto, California

- Occupation: Software Engineer at a tech startup

- Family: Single, with substantial disposable income

- Financial Goals: Long-term wealth accumulation with high growth potential, interested in sustainable tech.

- Aaron Davis

- Age: 31

- Location: San Francisco, California

- Occupation: Venture Capital Associate in a fintech firm

- Family: Recently married, with plans to start a family in 5+ years

- Financial Goals: Aggressive growth with a focus on tech-driven sustainable investments.

4.2 Understanding Client Information and KYC

4.2.1 Data Collection: Procedures for Gathering Essential Client Information

Effective data collection is the first critical step in the Know Your Client (KYC) process. This involves systematically gathering all relevant information about a client to form a comprehensive understanding of their financial status, investment experience, and goals. The process typically involves:

- Personal Identification: Collecting basic information such as name, address, date of birth, and identification numbers.

- Financial Information: Understanding the client’s financial situation including income, assets, liabilities, and existing investment portfolio.

- Investment Objectives and Risk Tolerance: Determining the client’s investment goals, time horizon, and risk appetite to ensure suitable investment advice.

- Employment Status and Background: Gathering information about the client’s profession and employment history, which can influence their investment strategy and risk profile.

Financial advisors use structured interviews, questionnaires, and direct documentation from clients to gather this data. This phase is crucial not only for compliance purposes but also for building a foundation on which tailored investment advice can be given.

4.2.2 Verification: Methods for Verifying the Accuracy and Authenticity of Client Information

Once data is collected, the next step is verification. This is essential to ensure the authenticity of the information provided and to protect against fraud. Methods include:

- Document Verification: Reviewing government-issued IDs, utility bills, bank statements, and other relevant documents to confirm the identities and addresses of clients.

- Background Checks: Conducting checks to verify employment status, financial history, and to screen for any criminal activities.

- Cross-Verification: Using third-party databases and credit bureaus to cross-check the information provided by the client.

Verification helps in mitigating risks associated with identity theft, financial fraud, and money laundering, ensuring that the financial institution complies with regulatory requirements.

4.2.3 Documentation: Keeping Records and the Importance of Updating Client Information Regularly

Maintaining accurate and up-to-date records of client information is a key component of KYC compliance. Effective documentation involves:

- Record-Keeping: Creating and maintaining files that contain all collected and verified information about the client. This includes digital records as well as hard copies where necessary.

- Regular Updates: Regularly updating client information to reflect any significant changes in their financial situation, investment objectives, or personal circumstances. This often involves periodic reviews and re-verification processes.

- Security and Confidentiality: Ensuring that all client data is stored securely, with access restricted to authorized personnel only, to protect client privacy and comply with data protection laws.

Regular documentation updates are vital not only for ongoing compliance with AML and KYC regulations but also for maintaining the accuracy of the financial advice provided. Changes in a client’s life, such as marriage, retirement, or changes in employment, can significantly affect their investment needs and risk tolerance.

The CFA curriculum emphasizes the importance of ethical and professional standards, which include diligent data collection, verification, and documentation as part of comprehensive client analysis. By adhering to these standards, investment professionals ensure they provide advice that accurately reflects each client’s circumstances and objectives.

4.3 Analyzing Client’s Investment Goals

In the process of crafting a tailored investment strategy, understanding the client’s specific financial goals is crucial. This understanding shapes how investment portfolios are designed and managed, ensuring alignment with the client’s needs, preferences, and life situation. Here’s how advisors can effectively analyze and incorporate client investment goals into their strategy formulation.

4.3.1 Identifying Short-term and Long-term Financial Goals

Financial goals can vary widely among individuals and typically fall into short-term and long-term categories. Each type of goal requires different investment strategies and risk considerations.

- Short-term Goals: These might include saving for a major purchase, such as a car or a wedding, within a few years. Investments aimed at fulfilling short-term goals are typically more conservative to preserve capital and ensure liquidity.

- Long-term Goals: These are often more substantial and might include retirement savings, purchasing a home, or funding a child’s education. Long-term goals allow for investing in vehicles with potentially higher returns, accepting higher volatility for greater growth over time.

Advisors work with clients to clearly define these goals, including the desired outcomes and the time frames for achieving them, which directs the choice of investment products.

4.3.2 Understanding Client’s Liquidity Needs and Time Horizon

Liquidity needs and investment time horizons are critical factors in developing an investment strategy:

- Liquidity Needs: Some clients require immediate liquidity for various reasons, such as business operations, upcoming expenditures, or emergency funds. These needs dictate a portion of the portfolio to be allocated in more liquid assets, even if it might offer lower returns.

- Time Horizon: The investment time horizon is closely tied to the client’s age, financial obligations, and risk tolerance. Longer horizons typically allow for investing in higher-risk, higher-return assets like stocks or real estate, as there is more time to recover from market fluctuations.

4.3.3 Considering the Client’s Life Stage and How It Influences Investment Objectives

A client’s life stage is a significant determinant of investment objectives:

- Early Career: Clients in the early stages of their career might focus on wealth accumulation and can afford to take higher risks due to a longer time horizon.

- Mid-Career: These clients may have more defined short-term goals with a moderate risk approach, balancing growth with income generation as they might be supporting a family or paying a mortgage.

- Pre-Retirement/Retirement: Clients nearing or in retirement will likely focus on income preservation and lower-risk investments, prioritizing stable, reliable returns and access to liquidity.

Understanding the nuances of each life stage helps advisors tailor strategies that not only aim to meet financial goals but also adapt to changing life circumstances and financial needs.

The CFA curriculum emphasizes the importance of suitability, which requires understanding the client’s financial situation, investment experience, and objectives. This suitability is a cornerstone of ethical and professional responsibility, ensuring that advisors recommend products that are appropriate for the client’s risk tolerance and investment horizon.

By carefully analyzing a client’s financial goals, liquidity needs, and life stage, advisors can construct personalized investment strategies that effectively address specific needs and preferences, ensuring clients are positioned to achieve their financial objectives efficiently and effectively.

All this information can be gathered in various ways. Below find examples for interview questions and answers for the two client examples.

1. Conservative Swiss Client

Liquidity Needs:

- Question: “Do you anticipate needing significant access to your investments within the next few years?”

- Question: “Are there specific life events (e.g., property purchase, children’s needs) where you’ll require funds?”

- Answer: “I don’t expect any major expenses in the next few years, but I’d like some flexibility in case of emergencies or family support needs.”

- Liquidity Requirement: Moderate. This allows for a modest cash allocation or short-term bonds to maintain some liquidity.

Time Horizon:

- Question: “What is your investment timeframe? Are you aiming for steady income in retirement or growth over the next few years?”

- Answer: “I plan to retire in about 10-15 years and want to have a stable income by then. My focus is on safe, long-term growth until retirement.”

- Time Horizon: Medium-to-long-term (10-15 years). Allows a stable income focus through bonds and limited equities.

Income Requirements:

- Question: “Are you seeking regular income from this portfolio for personal expenses?”

- Question: “What percentage of your portfolio would you expect to generate income versus appreciation?”

- Answer: “Yes, I’d like this portfolio to generate some income, though capital preservation is still my priority.”

- Income Needs: Income-focused. Requires dividend-paying stocks or bonds to produce consistent returns.

2. Dynamic US ESG Client

Liquidity Needs:

- Question: “Do you need regular access to funds for expenses, or are you able to hold investments over a long horizon?”

- Question: “Would you want a portion of your portfolio accessible for potential opportunities or unforeseen needs?”

- Answer: “I don’t need much liquidity at the moment. I can afford to reinvest and wait for growth.”

- Liquidity Requirement: Low. Permits a more illiquid portfolio with minor cash allocations.

Time Horizon:

- Question: “How long do you plan to stay invested before drawing down on these funds?”

- Answer: “I plan to invest for at least 20 years. I’m focused on long-term growth.”

- Time Horizon: Long-term (20+ years). Suits growth-focused assets with higher volatility.

Income Requirements:

- Question: “Do you expect this portfolio to generate income, or are you more focused on capital growth?”

- Answer: “I don’t need income now; I’d rather the portfolio grow as much as possible.”

- Income Needs: Minimal. Allows for growth-focused investments, potentially including reinvested dividends.

4.4 Assessing Risk Tolerance

Assessing risk tolerance is fundamental in the client analysis process, crucial for aligning investment strategies with the client’s comfort level regarding potential financial loss. It involves a combination of qualitative discussions and quantitative assessments to gauge how much risk a client is willing to accept in pursuit of their financial goals.

4.4.1 Methods for Evaluating Client’s Risk Appetite

- Questionnaires: Structured questionnaires are commonly used to quantify risk tolerance. These may include scenarios that help clients consider potential losses and gains, and gauge their reactions to different market conditions. These tools help standardize the assessment process and provide a baseline measure of risk tolerance that can be revisited and compared over time.

- Interviews: Personal interviews provide deeper insights into the client’s attitudes towards risk. Through discussions, advisors can understand the reasons behind a client’s investment decisions, their previous investment experiences, and their emotional responses to market fluctuations. This qualitative method complements the quantitative data gathered through questionnaires.

4.4.2 Psychological Aspects of Risk Tolerance

Understanding the psychological underpinnings of risk tolerance is crucial for crafting a strategy that clients are comfortable with and that keeps them engaged in the long term.

- Behavioral Biases: Cognitive biases such as loss aversion, overconfidence, or recency bias can significantly influence a client’s perceived risk tolerance. For example, a client might overestimate their tolerance for risk during market upswings but become highly risk-averse during downturns.

- Emotional Factors: The emotional capacity to handle the stress of volatile investments varies widely among individuals. Some may prefer the potential for higher returns despite the possibility of significant volatility, while others might prioritize stability to avoid anxiety.

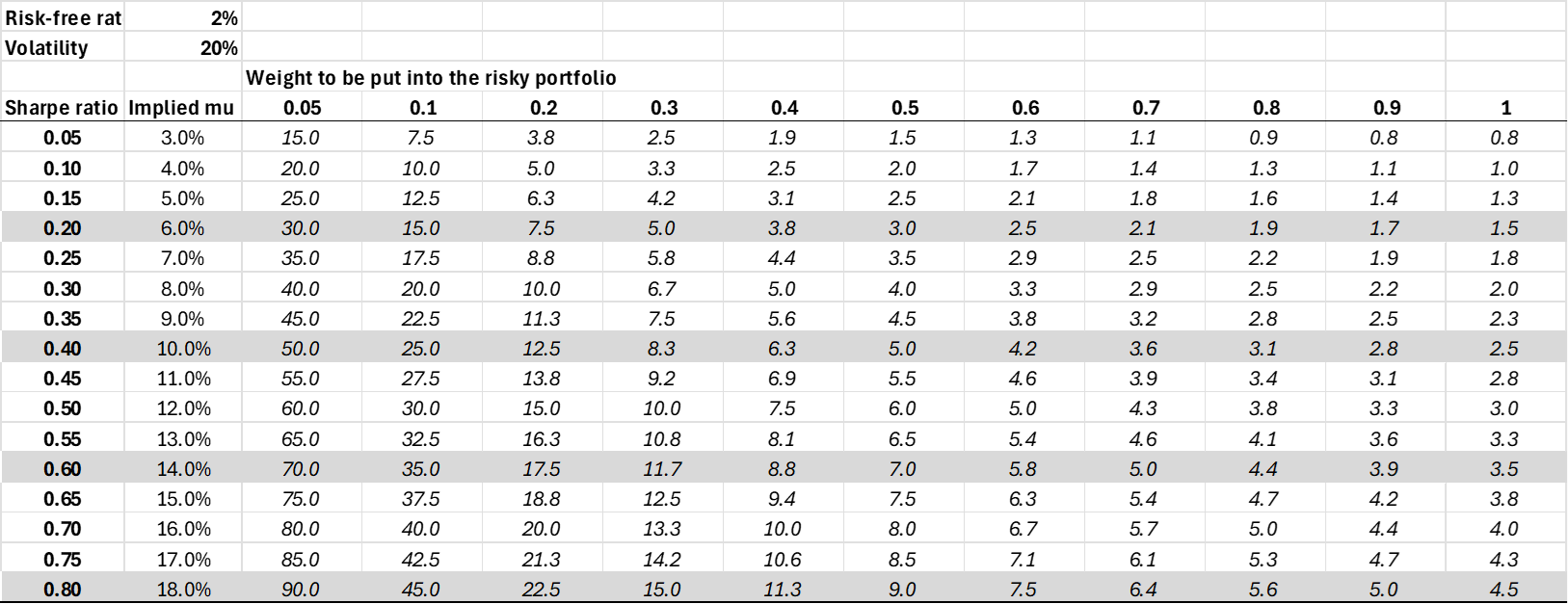

4.4.3 Determining the level of risk aversion: An experiment

In the following exercise, the client has to answer certain questions (without looking at the entire table).

Given a risk-free rate of 2% and a market volatility of 20%: “What percentage of your wealth would you allocate to the risky investment portfolio (the market).”

- Assume a Sharpe ratio of 0.2 which means, the market is paying a (excess) return of (4%) 6%.

\(\rightarrow\) Answer: “I would certainly allocate between 20% and 30% of my wealth to risk investments” (yielding a risk aversion of 5-7.5)

- Assume now, that the market’s Sharpe ratio would be 0.60, yielding a (excess) return of (12%) 14%.

\(\rightarrow\) Answer: “In this case I would allocate about 60% of my wealth to risky assets” (thereby yielding a risk aversion of 5.8)

In sum, the risk aversion in this simple example would be set to 6.

4.4.4 Matching Risk Tolerance with Investment Strategies

Once risk tolerance is assessed, it is crucial to match it with suitable investment strategies and asset allocations:

- Conservative Strategies: For clients with low risk tolerance (risk aversion above 6-8), conservative strategies focus on preserving capital and generating steady, low-risk returns. This might include higher allocations to bonds, money market funds, or stable dividend-paying stocks.

- Moderate Strategies: Clients with a moderate risk tolerance (risk aversion between 3 and 6) may be comfortable with a balanced approach that includes a mix of equities and fixed-income securities. This strategy aims to achieve a reasonable rate of return by accepting moderate levels of risk.

- Aggressive Strategies: High-risk tolerance clients (risk aversion below 3) might be suited for aggressive investment strategies, which primarily focus on capital appreciation. This often involves higher allocations to stocks, especially in sectors with higher volatility and potential for substantial growth, such as technology or emerging markets.

The CFA curriculum emphasizes the importance of aligning investment strategies with client risk tolerance, a key component of ethical and professional standards in financial advice. It teaches that understanding and accurately assessing risk tolerance is essential not only for client satisfaction but also for adherence to fiduciary responsibilities.

4.4.5 The Role and Impact of Uncertainty

By meticulously assessing a client’s risk tolerance and understanding its psychological basis, advisors can ensure that the recommended investment strategies genuinely meet the client’s needs and preferences, thereby fostering trust and long-term client engagement.

After interviewing clients and testing for their risk tolerance, we find the results below. Further questions and experiments reveal additional information on the risk budgets of the individuals.

1. Conservative Swiss Client

Risk Tolerance and Capacity:

- Question: “On a scale from 1 to 10, how comfortable are you with short-term fluctuations in your portfolio value?”

- Question: Do you prefer stable, predictable returns even if they’re lower, or are you open to some volatility for potentially higher returns?”

- Answer: “I’m uncomfortable with large fluctuations. I prefer steady growth, even if the returns are lower. Stability is more important than maximizing returns.”

- Risk Tolerance: Low. This translates to a high allocation in stable assets like government and investment-grade corporate bonds.

- Risk Aversion Coefficient: A = 6 (High risk aversion).

Risk Budgets:

- VaR (95%): Limit to 10% potential loss over a one-month period.

- CVaR (Expected Shortfall): Cap at 15% for extreme cases.

- Maximum Drawdown: Up to 20% peak-to-trough decline allowed.

Currency Allocation:

- Question: “Which currencies do you feel familiar to?”

- Question: “Which currencies do you feel uncertain about and do you probably want to avoid?”

- Currency Strategy:

- Christine’s comfort with foreign assets is limited by perceived risks in unfamiliar currencies.

- She expresses a desire for some foreign exposure but would prefer it to be minimized, especially in regions with potential currency volatility.

- Christine is more open to USD exposure, viewing the U.S. as relatively stable economically and politically.

2. Dynamic US ESG Client

Risk Tolerance and Capacity:

- Question: “Are you comfortable with substantial short-term losses for the potential of long-term gains?”

- Question: “How important is stability versus potential growth in your portfolio?”

- Answer: “I’m okay with volatility if it means higher returns. Short-term losses don’t bother me as long as the long-term growth potential is there.”

- Risk Tolerance: High. Allows for a significant allocation in high-yield equities, corporate bonds, and potentially higher volatility assets.

- Risk Aversion Coefficient: A = 2.5 (Lower risk aversion).

Risk Budgets:

- VaR (95%): Limit to 5% potential loss over a one-month period.

- CVaR (Expected Shortfall): Cap at 7% loss for extreme cases.

- Maximum Drawdown: 10% limit on peak-to-trough decline.

Currency Allocation:

- Question: “Which currencies do you feel familiar to?”

- Question: “Which currencies do you feel uncertain about and do you probably want to avoid?”

- Currency Strategy:

- Jake is comfortable with global diversification but prefers to balance this with exposure in stable regions.

- He sees the USD as a core currency but is intrigued by EUR for European green tech investments and emerging ESG markets.

- Less familiar with CHF and JPY, he would only allocate to these currencies if there is a compelling ESG or tech-related opportunity.

4.5 Identifying Rate of Return Requirements

Accurately identifying a client’s rate of return requirements is essential for devising an investment strategy that aligns with their financial goals, risk tolerance, and time horizon. This process involves calculating the target rate of return necessary to meet specific financial objectives within a defined time frame, while also considering market conditions and the client’s risk profile.

4.5.1 Calculating the Client’s Target Rate of Return

- Understanding Financial Goals: The first step is to define and quantify the client’s financial goals, whether it’s saving for retirement, buying a home, funding education, or building an emergency fund. Each goal requires estimating the future cost and the time frame for achieving it.

- Required Rate of Return Calculation: Once the goals are clearly defined, calculate the rate of return needed to achieve these goals from the current investment base. This involves using financial formulas that incorporate the initial investment amount, the goal amount, the time horizon, and the effects of compounding. Financial planning software or calculators can be used to simplify these calculations.

Example formula: \[\text{Required Rate of Return} = (\frac{\text{Future Value}}{\text{Present Value}})^\frac{1}{n} - 1\] where n is the number of periods until the goal must be reached.

Experiment 1: Return Expectation Interview Questions

This experiment uses scenario-based questions to help clients articulate their desired return based on hypothetical situations. It can reveal not only their expected rate of return but also their willingness to adjust their expectations according to risk levels.

Scenario-Based Questions:

- Scenario A: “Imagine you invest $100,000. How would you feel about a steady annual return of 4% over 10 years, resulting in approximately $48,000 in growth? Is this return in line with what you expect, or would you prefer something higher, even if it involves more risk?”

- Scenario B: “Suppose you could achieve a 6% return, which involves moderate risk and some annual fluctuations, potentially losing 5% in a given year but gaining 10% in another. Would this match your financial objectives, or would you still consider it too risky or too low?”

- Scenario C: “Now imagine a scenario where you aim for an 8% return per year, but there is a high likelihood of seeing more significant fluctuations in value, with occasional drops of up to 15% in a given year. Does this match your financial objectives, or does it feel too volatile?”

Based on the client’s comfort level with each scenario, the advisor can gauge whether the client’s required rate of return is in the conservative, moderate, or aggressive range. For instance, if the client only feels comfortable with Scenario A, they may have a required return around 4%, reflecting a conservative objective. If they lean toward Scenario C, an 8% required return might align better with their risk tolerance and expectations.

Experiment 2: Goal-Based Return Requirement Calculation

In this exercise, the client sets specific financial goals, and the advisor calculates the required rate of return to meet those goals. This method is particularly useful for clients with clearly defined financial objectives and timelines, such as retirement savings, a home purchase, or college tuition.

Steps:

- Identify Goals and Time Horizon: Ask the client to state a financial goal, such as “I want to have $500,000 saved in 15 years for retirement.”

- Assess Current Savings and Contributions: Determine how much the client has already saved and what they can contribute annually toward this goal.

- Calculate Required Rate of Return: Using the Future Value of an Investment formula, calculate the rate of return needed to reach the goal.

Formula: \[FV = PV \times (1 + r)^n + \text{annual contributions}\] Rearranging to solve for r (required rate of return): \[r = \left( \frac{FV}{PV + \text{annual contributions}} \right)^{\frac{1}{n}} - 1\]

Example Calculation:

If Christine has $200,000 saved and wants to reach $500,000 in 15 years by contributing $5,000 annually, the required rate of return can be calculated. Adjusting her portfolio to meet this target rate helps guide asset allocation decisions.

Interview Question: Rate of Return Preferences

Finally, you can use direct interview questions to understand a client’s return expectations:

- “What rate of return do you believe is necessary for you to meet your financial goals?”

- This can help capture the client’s implicit return target, allowing you to compare it with market expectations and their risk profile.

- “Would you be comfortable with a lower return if it meant more stability, or do you prioritize achieving a high return, even if it comes with higher risks?”

- This question can provide insights into the client’s risk-return trade-off preference.

- “Given your goals, would you consider a flexible strategy where your return expectations adjust with market conditions, or do you expect a consistent return target?”

- This helps to establish if the client is adaptable or requires a fixed target, impacting strategic asset allocation flexibility.

4.5.2 Balancing Return Targets with Market Realities

- Market Expectations: It’s crucial to align the calculated target rate of return with realistic market expectations. Historical data, economic forecasts, and current market conditions should be analyzed to estimate feasible returns from different asset classes over the investment period.

- Risk Considerations: There must be a balance between the desired rate of return and the level of risk the client is willing and able to take. Higher returns typically come with higher risk, and the client’s risk tolerance assessed earlier will guide how much risk is appropriate.

- For lower risk tolerance: Focus on conservative investments such as bonds or stable value funds which generally offer lower but more predictable returns.

- For higher risk tolerance: Consider more volatile investments such as stocks or mutual funds focused on growth sectors, which could potentially offer higher returns but with greater risk and volatility.

The CFA curriculum includes extensive coverage on how to integrate client-specific factors such as financial goals and risk tolerance into personalized investment advice. It teaches that financial advisors must not only aim to achieve the mathematical target rate of return but also consider the client’s overall financial situation, market conditions, and psychological comfort with risk levels.

4.5.3 Conclusion

Determining a client’s rate of return requirements is a critical task that bridges their financial aspirations with practical investment strategies. By thoroughly understanding their goals, calculating necessary returns, and realistically aligning these with market conditions and personal risk profiles, advisors can develop strategies that are both achievable and aligned with the client’s financial health and life priorities. This disciplined approach ensures that investment recommendations are not only theoretically sound but also practically viable and tailored to individual needs.

For our clients we did not evaluate required rates of return

1. Conservative Swiss Client

Required Rate of Return:

- Scenario A (4% annual return, low risk): “This sounds appealing. I prefer stability and preserving my capital with some growth, even if returns are modest.”

- Scenario B (6% annual return, moderate risk): “I would consider this if it means better returns, but I would need reassurance that the risk is manageable.”

- Scenario C (8% annual return, higher risk): “This is too risky for me. I don’t want to see large fluctuations, especially as I approach retirement.”

Based on Christine’s responses, she leans toward Scenario A, indicating a conservative to moderately conservative return target.

- Goal: Christine wants to retire with CHF 1,000,000 in 15 years.

- Current Savings: CHF 500,000

- Annual Contributions: CHF 10,000

Using the Future Value formula, we can calculate her required rate of return to be 3.2%, aligning well with her conservative profile.

Lottery-Based Risk Aversion: Christine consistently prefers the safer, lower-return options, which corresponds to a high risk aversion coefficient (around 5-7). This is compatible with her conservative risk tolerance.

Return Requirement: Targeting 3-4% annually

2. Dynamic US ESG Client

Required Rate of Return:

- Scenario A (4% annual return, low risk): “This is too conservative for me. I’m young and have time to recover from market downturns.”

- Scenario B (6% annual return, moderate risk): “This is closer, but I’m still looking for a bit more growth potential.”

- Scenario C (8% annual return, higher risk): “This aligns with my goals. I want to aim for higher returns, even if it means facing more risk.”

Alex’s responses indicate a preference for Scenario C, supporting an aggressive return target.

- Goal: Alex aims to grow his portfolio to $2,000,000 in 25 years.

- Current Savings: $100,000

- Annual Contributions: $15,000

Calculating Alex’s required rate of return as 6.5%, which matches his higher risk tolerance.

Lottery-Based Risk Aversion: Alex consistently chooses higher-return, riskier options, showing a low risk aversion coefficient (around 1.5-3). He is comfortable with high volatility and risk.

Return Requirement: Targeting 6-8% annually

4.6 Other Client Requirements and Constraints

In addition to risk tolerance and rate of return requirements, a comprehensive investment strategy must also consider various other client-specific requirements and constraints. These include legal and tax considerations, liquidity needs, ethical and social constraints, and regulatory requirements. Addressing these factors is crucial for creating a tailored and compliant investment plan.

4.6.1 Legal and Tax Considerations

- Legal Framework: Legal considerations can significantly influence investment decisions, especially regarding the ownership structure, inheritance laws, and cross-border investment regulations. For instance, legal restrictions might limit investment opportunities in certain countries or industries, impacting portfolio diversification.

- Tax Implications: Tax considerations are critical in investment planning as they affect the net return on investments. Different investment vehicles and strategies can have varied tax implications, including income tax, capital gains tax, and estate tax. Advisors must be proficient in optimizing investment strategies to take advantage of tax incentives, defer taxes, or minimize tax liabilities, always in compliance with current legislation.

- Example: Utilizing tax-advantaged accounts like IRAs or 401(k)s for retirement savings or considering tax-free municipal bonds for taxable accounts.

4.6.2 Liquidity Needs

Understanding a client’s liquidity needs involves recognizing the necessity for readily accessible funds to cover short-term expenses or emergencies without compromising the long-term investment strategy. - Cash Flow Management: Advisors must ensure there is enough liquidity in the portfolio to meet anticipated expenses such as tuition fees or scheduled debt repayments. - Emergency Funds: It is advisable to maintain an emergency fund that covers 3-6 months of living expenses in easily accessible accounts like savings accounts or money market funds.

4.6.4 Regulatory Requirements

Investment advisors must navigate a complex landscape of industry and government regulations that influence what financial products can be offered to clients and how those products can be managed.

- Compliance with Regulations: This includes adhering to regulations set forth by bodies such as the Securities and Exchange Commission (SEC) or Financial Industry Regulatory Authority (FINRA) in the U.S., which govern securities transactions and protect investor interests.

- Client Protection Standards: Advisors must ensure that all investment recommendations comply with suitability standards that require a good faith effort to act in the client’s best interest.

For our clients we did not evaluate required rates of return

1. Conservative Swiss Client

ESG and Ethical Constraints:

- “I am not specifically focused on sustainability aspects, so I would prefer a traditional approach without any ESG weighting adjustments.”

- ESG Strategy: No preference for ESG adjustments, allowing for a conventional allocation without incorporating ESG-driven returns.

2. Dynamic US ESG Client

ESG and Ethical Constraints:

- “I’m interested in sustainability but only if it aligns with my growth objectives. If a company improves its ESG score, I’d expect a performance boost; otherwise, I don’t need the investment to have a high ESG level from the start.”

- ESG Strategy: Prefers an ESG-change model that rewards improvements in ESG scores (upgrades) with higher returns and penalizes downgrades, integrating sustainability with growth potential.

4.6.5 Conclusion

By carefully considering these additional constraints and requirements, financial advisors can ensure that the investment strategies they develop are not only aligned with their clients’ financial goals but also with their legal, ethical, and personal circumstances. This holistic approach to client analysis ensures that the investment plan is robust, compliant, and truly personalized, fostering long-term relationships and client satisfaction.

4.7 Conclusion: The Essential Role of Client Analysis in Financial Advisory

4.7.1 The Foundation of Client-Advisor Relationships

Client analysis is not merely a procedural task—it’s the cornerstone of a successful client-advisor relationship. This comprehensive process involves understanding the client’s financial goals, risk tolerance, legal constraints, tax considerations, and personal values. By gaining a deep insight into these areas, financial advisors can tailor strategies that are not only effective in achieving financial objectives but also resonate with the client’s personal and ethical standards. This alignment is crucial for building trust and confidence, which are the bedrocks of a long-lasting advisory relationship.

4.7.2 Dynamic Nature of Client Analysis

The financial world is not static, and neither are clients’ lives. Economic conditions change, financial markets fluctuate, and personal circumstances evolve. As such, client analysis is a dynamic process. It requires ongoing review and adaptation to remain relevant and effective. Regularly revisiting the client’s financial situation and goals allows advisors to adjust investment strategies as needed, ensuring that they continue to meet the client’s current needs while also anticipating future changes.

- Periodic Reviews: Scheduled reviews, whether annually or biannually, help keep the client’s financial strategy aligned with their evolving goals and changing market conditions.

- Adaptability: Being adaptable in strategy formulation enables advisors to respond swiftly to significant life events such as marriage, childbirth, career changes, or retirement, which might alter a client’s financial trajectory and risk profile.

4.7.3 Proactive Approach to Client Needs

Advisors are encouraged to adopt a proactive approach in managing client relationships. This involves: - Anticipating Changes: Staying informed of potential changes in the client’s life and in the regulatory or economic landscape that could impact their investments. - Communication: Maintaining open lines of communication with clients to discuss their concerns and aspirations, and to ensure they are informed about how their portfolios are being managed. - Education: Keeping clients educated about investment options and market dynamics helps them make informed decisions and fosters a collaborative relationship.

4.7.4 Encouragement for Advisors

As financial landscapes become increasingly complex and client expectations grow, the role of client analysis becomes more critical than ever. Advisors are encouraged to view client analysis not just as due diligence but as an ongoing opportunity to deepen client relationships. Through meticulous and empathetic client analysis, advisors can provide personalized, informed, and strategic advice that meets clients where they are and helps them get to where they want to be.

4.7.5 Final Thoughts

In conclusion, effective client analysis is essential for crafting personalized investment strategies that achieve clients’ financial goals while respecting their risk tolerance and personal values. By continuously engaging in this process, advisors can ensure that their advice remains pertinent and valuable, reinforcing the client’s trust and securing their financial future. This proactive and dynamic approach in client analysis underscores the advisor’s commitment to service excellence and client satisfaction, paving the way for enduring partnerships and mutual success.