3 Sustainable Investing

Associated slides: Lesson 2 — Markets, Asset Classes & ESG

3.1 Introduction

3.1.1 Defining Sustainable Investing and Its Growing Importance

Sustainable investing refers to the practice of incorporating environmental, social, and governance (ESG) factors into investment decisions to help generate long-term competitive financial returns and positive societal impact. According to the Global Sustainable Investment Alliance (GSIA), sustainable investing assets reached $35.3 trillion at the start of 2020, which represents 36% of all professionally managed assets across regions covered by GSIA’s biennial report. This demonstrates a significant growth from $22.8 trillion in 2016, underscoring the increasing importance of ESG considerations in investment practices globally.

The concept of sustainable investing has been formalized through various frameworks and definitions, one of the most notable being the Principles for Responsible Investment (PRI). Initiated in 2006 with the support of the United Nations, PRI has evolved into a network of more than 3,000 signatories (as of 2021), managing over $100 trillion in assets, who commit to integrate ESG factors into their investment and ownership decisions.

The financial relevance of sustainable investing is further supported by numerous studies demonstrating its impact on investment performance. For example, a meta-study by the University of Oxford and Arabesque Partners reviewed more than 200 sources and found that 80% of the research showed that good sustainability practices positively influenced stock price performance. Moreover, regulatory trends, such as the EU’s Sustainable Finance Disclosure Regulation (SFDR) implemented in March 2021, have propelled the importance of transparency in how companies and funds integrate ESG factors, reflecting an institutional shift towards embedding sustainability in financial analysis.

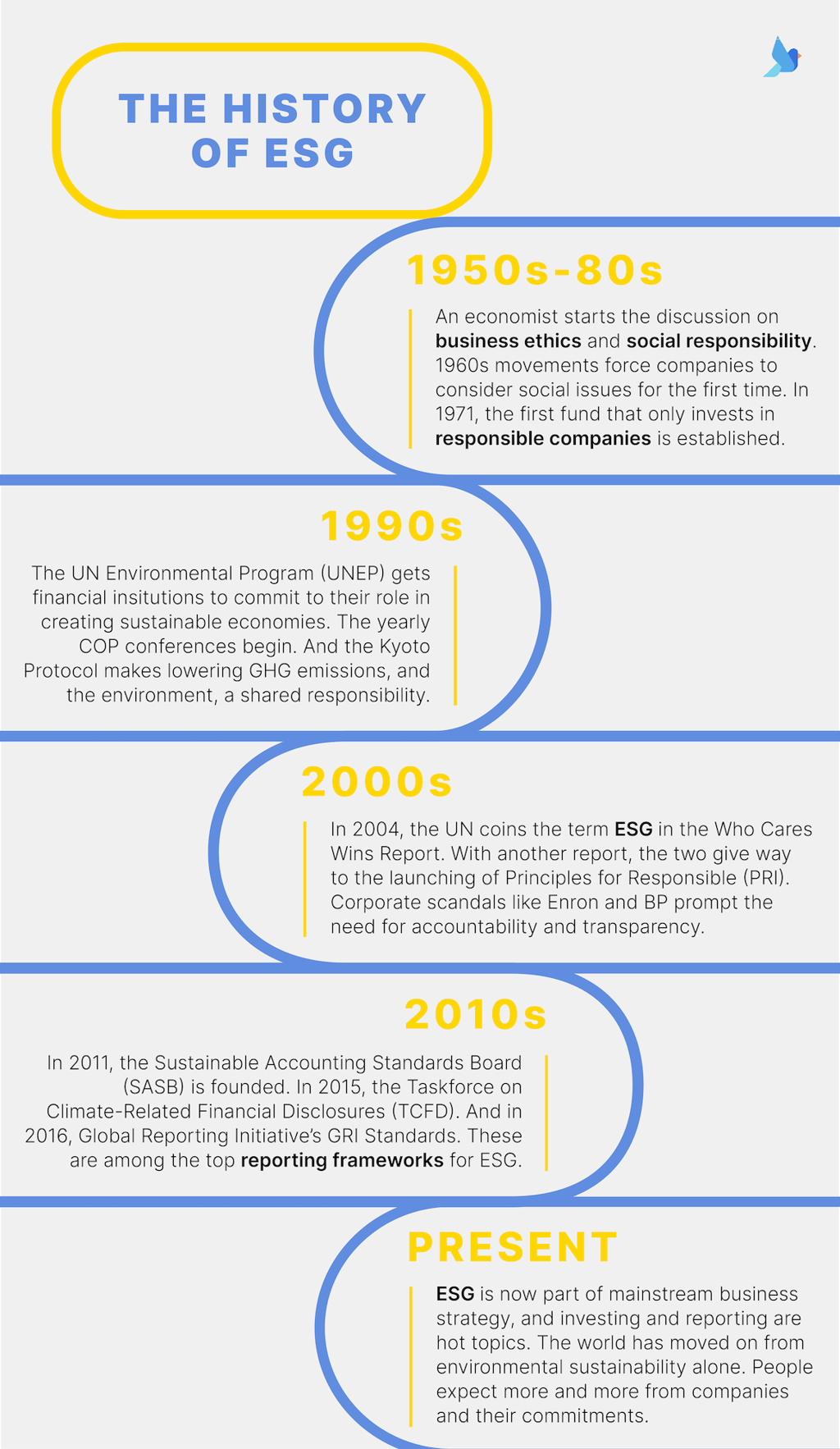

3.1.2 The Evolution of Sustainable Investing: From Niche to Mainstream

Sustainable investing has transformed from a peripheral interest to a central focus in the financial industry, reflecting a profound shift in investor values and market strategies. Initially perceived as a practice aligned primarily with moral and ethical considerations, sustainable investing was often confined to exclusionary screens that avoided investments in industries such as tobacco, firearms, and fossil fuels. This approach, however, has significantly evolved over the years.

The 1990s marked the beginning of a new era for sustainable investing with the introduction of the Dow Jones Sustainability Index (DJSI) in 1999, one of the first global indices to track the performance of leading sustainability-driven companies worldwide. This was a pivotal moment that signaled the integration of ESG criteria into mainstream financial analysis, showcasing that sustainable investing could align investor values with financial performance.

By the 2010s, sustainable investing had gained substantial momentum, underscored by global initiatives such as the United Nations’ Sustainable Development Goals (SDGs) established in 2015 and the Paris Agreement on climate change. These frameworks provided a clear set of objectives for addressing global challenges, which in turn catalyzed further interest and investment in sustainable practices. As of 2020, an estimated 33% of total U.S. assets under management are being invested according to sustainable investment strategies, highlighting the mainstream acceptance of this approach.

3.1.3 Financial and Ethical Motivations Behind Sustainable Investing

The motivations driving sustainable investing are multifaceted, encompassing both financial pragmatism and ethical considerations. From a financial perspective, investors are increasingly aware that ESG factors can significantly influence risk and return profiles. A study by MSCI in 2019 found that companies with strong ESG ratings exhibited higher profitability, lower tail risk, and were less volatile than their lower-rated counterparts. This financial rationale is complemented by the ethical motivation to generate positive social and environmental impact alongside financial returns.

Ethically, investors are motivated by the desire to contribute to societal well-being and environmental sustainability. This is particularly evident among younger generations, such as millennials, who not only prefer to invest in companies that reflect their social and environmental values but also demand greater transparency and accountability in how their money is managed.

Furthermore, as global challenges like climate change and social inequality intensify, the ethical imperative for sustainable investing becomes even more pronounced. Investors are using their capital to influence corporate behaviors and fund projects that support sustainable economic development, clean energy transitions, and equitable social progress.

3.2 Measuring Sustainability in Companies

3.2.1 How to Quantify Sustainability

To quantify sustainability, investors and analysts use Environmental, Social, and Governance (ESG) criteria to assess how well a company manages key areas that could impact its financial health and operational success. Environmental criteria consider how a company performs as a steward of nature. Social criteria examine how it manages relationships with employees, suppliers, customers, and communities. Governance deals with a company’s leadership, executive pay, audits, internal controls, and shareholder rights.

- Environmental Aspect: Includes the company’s energy use, waste management, resource conservation, and treatment of animals. The metrics also assess any environmental risks a company might face and how these risks are managed.

- Social Aspect: Focuses on the company’s business relationships. Does it work with suppliers that hold the same values it claims to hold? Does the company donate a percentage of its profits to the local community or encourage employees to perform volunteer work?

- Governance Aspect: Pertains to a company’s leadership, executive pay, audits, internal controls, and shareholder rights.

The quantification of these factors often involves the use of sustainability indexes or ratings provided by global institutions.

3.2.2 Evolution of ESG Scores

The concept of integrating social and environmental considerations into investment decisions began to take shape in the 1960s and 1970s, primarily driven by the social justice movements of the time. These early forms of what would eventually become ESG investing were largely focused on exclusionary screening, avoiding investments in businesses involved with the South African apartheid regime, as well as in tobacco, alcohol, and defense industries.

In the late 1980s and early 1990s, the first tools to help investors assess a company’s environmental impact and social governance began to emerge. 1990 marked a significant milestone with the launch of the Domini 400 Social Index (now the MSCI KLD 400 Social Index), one of the first indices intended to help investors benchmark the performance of companies with superior ESG ratings.

The Role of Major Players and Expansion:

- MSCI: A pivotal player in ESG scoring, MSCI started providing ESG ratings in 2010 after acquiring RiskMetrics and Innovest, which had begun exploring financially material ESG issues in the early 2000s. MSCI’s ratings now influence trillions of dollars in assets, guiding the strategies of global investors.

- S&P Global: Entered the ESG space more robustly in 2018 by acquiring Trucost, a company renowned for its detailed environmental data and risk analysis. S&P Global provides detailed ESG scores and has integrated ESG into its broader market indices.

- Bloomberg: Began offering ESG data services in 2009, which have since become a key resource for investors looking to integrate sustainability metrics into their analysis.

The adoption of ESG scores has seen exponential growth, particularly over the past decade. According to the Global Sustainable Investment Review, sustainable investment now tops $30 trillion—up 68% since 2014 and tenfold since 2004. ESG metrics have been increasingly embraced not only by specialized ESG funds but also by traditional funds seeking to enhance risk assessment and identify growth opportunities aligned with sustainability trends.

The number of ESG funds has surged, with Morningstar reporting that there were over 3,432 ESG funds at the end of 2020, representing a significant increase from just a few hundred a decade earlier. These funds utilize ESG scores to shape their investment portfolios, often using scores provided by major agencies like MSCI or S&P Global to screen potential investments and manage ongoing compliance with their sustainability criteria.

The growing reliance on ESG scores has not only influenced how assets are allocated but also pushed companies to improve their practices in order to attract investment. For instance, a survey by the CFA Institute indicated that 76% of investors consider ESG factors in their investment analysis, pointing to a robust integration of these criteria into mainstream financial analysis.

3.2.3 Key Providers of ESG Scores

| Rating Provider | Type of Scores and Ratings | Rating Range |

|---|---|---|

| MSCI | ESG Ratings assess resilience to long-term ESG risks. | AAA - CCC (Leader to Laggard) |

| S&P Global | ESG Evaluation scores (Strategy + Preparedness). | 0 - 100 |

| Bloomberg | Comprehensive data points (not a single score). | No specific scale; raw data. |

| RobecoSAM | Corporate Sustainability Assessment (CSA). | Percentile rankings relative to peers. |

| Refinitiv | ESG performance, commitment, and effectiveness. | 0 - 100 (Normalized by industry) |

| Sustainalytics | ESG Risk Ratings (Economic value at risk). | 0 - 50 (Lower score = Lower risk) |

In IMAG we use ESG (sub-)scores in the range 0-100. Those scores can change over time.

3.3 Sustainability Across Asset Classes

3.3.1 Equities

When evaluating equities, assessing a company’s sustainability involves a detailed analysis of environmental, social, and governance (ESG) factors. This analysis helps investors understand how a company manages risks and opportunities related to sustainable practices. The sustainability performance of companies, as reflected by their ESG scores, is increasingly seen as an indicator of operational and financial efficiency. High ESG scores are associated with better risk management and more sustainable growth opportunities, which can lead to enhanced profitability and valuation. According to research by Friede, Busch, and Bassen (2015), which aggregated evidence from more than 2,000 empirical studies, there is a positive correlation between ESG performance and financial performance, evident across various sectors and regions. This evidence suggests that companies with high ESG scores tend to experience lower costs of capital and less volatility, which are attractive qualities for equity investors.

In IMAG, depending on the type of financial scenario played, as well as the simulation, there are two possible scenarios where ESG might have an impact on a stock’s performance:

- Level of ESG rating: higher/lower ESG ratings can be accompanied by higher or lower annual returns, reflecting the idea that (1) higher sustainability goes hand in hand with higher cost and therefore lower performance or (2) the idea that higher ESG ratings reflect a more stable company that is better adapted to future challenges.

- Change in ESG rating: a positive/negative change in ESG rating reflects increased investor attention as well as eligibility of the stock for ESG investment funds which goes hand in hand with a one-time positive/negative return.

3.3.2 Corporate Bonds

ESG Scores and Corporate Bond Performance: Corporate bonds issued by companies with high ESG scores can be perceived as lower risk compared to those from companies with poor ESG performance. This perception can lead to more favorable credit ratings and lower yield spreads. However, the ESG score of a company does not always directly translate to each bond issuance. For instance, green bonds, which are specifically intended to fund projects with positive environmental benefits, might carry different risk assessments and ratings despite being issued by the same entity.

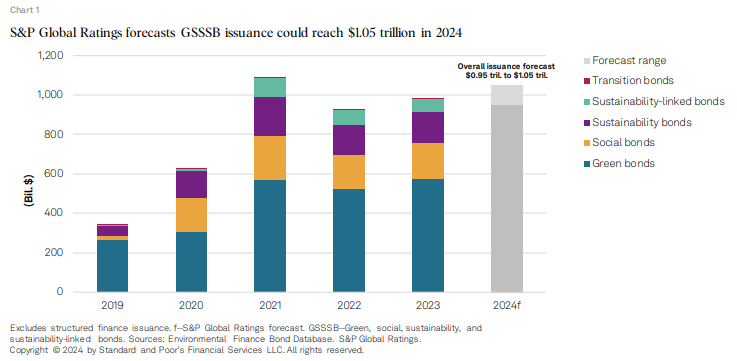

Green Bonds: Green bonds are an interesting case where the use of proceeds is strictly earmarked for environmental projects, potentially aligning with high corporate ESG scores but also carrying their own distinct evaluations. These bonds have surged in popularity, with the global green bond issuance reaching $258.9 billion in 2019, according to the Climate Bonds Initiative. Investors often favor green bonds not only for their intended environmental impact but also for their potential to mitigate risk associated with climate change, providing a dual benefit of financial return and positive environmental impact.

Role of Sustainability in Credit Risk and Bond Yields:: Incorporating sustainability into credit risk assessment can alter a bond’s yield. Bonds issued by companies with poor ESG practices may carry higher risk and consequently higher yields to compensate investors. Conversely, green bonds might offer lower yields due to their lower risk profile and strong demand from socially responsible investors. The perception of lower default risks associated with sustainable projects can enhance the creditworthiness of issuers.

3.3.3 Government Bonds

Relation of ESG to Government Bonds: Government bonds do not typically carry ESG scores in the same manner as corporate entities; however, the principles of sustainable investing are increasingly applicable at the sovereign level. Investors might evaluate the sustainability of government bonds based on the country’s environmental policies, social governance, and economic management. Countries with robust sustainable policies and practices can be seen as lower risk, potentially leading to more favorable borrowing terms in the bond market.

Interesting Fact: Countries like Sweden and France have issued green bonds that fund national environmental and sustainability projects, reflecting a commitment to climate action and sustainable development, which resonates well with socially responsible investors.

Suggested Visuals and Additional Information: - Correlation Chart: A graph illustrating the correlation between high ESG scores and lower costs of capital, based on the findings by Friede, Busch, and Bassen. - Case Study of a Green Bond: Highlighting a specific green bond issuance, detailing the environmental projects it funds and its financial performance.

3.3.4 Commodities

Sustainable Practices in Commodity Production and Extraction: The sustainability of commodity production is increasingly scrutinized due to the significant environmental and social impacts associated with mining and agriculture. Companies in the commodity sector that maintain high ESG standards tend to employ advanced technologies and strategies to minimize environmental damage and ensure responsible social practices. This can include reducing greenhouse gas emissions, ensuring fair labor practices, and engaging in community development. Investors often use ESG scores to assess the commitment of commodity-producing companies to sustainability, which can influence their investment decisions.

Ethical Sourcing and Its Impact on Commodity Prices: Ethically sourced commodities are becoming increasingly valued not only for their reduced environmental impact but also for their ability to meet consumer demand for sustainability. Commodities such as conflict-free minerals, sustainably harvested timber, and organically grown agricultural products often command premium prices in the market. The traceability and certification of these commodities, verified by credible ESG scores, can lead to a price premium, reflecting the higher consumer willingness to pay for products that are ethically produced.

Interesting Fact: The Responsible Jewellery Council certifies gold and other precious metals that are mined and processed following high sustainability standards, which can enhance their marketability and price stability.

3.3.5 Cryptocurrencies

Debate on the Environmental Impact of Cryptocurrency Mining: Cryptocurrencies, especially Bitcoin, have been under scrutiny for the substantial energy consumption required for mining operations, which often rely on non-renewable energy sources. The ESG implications are significant, as the carbon footprint associated with mining could negate the benefits of using digital currency. However, there is a growing movement within the cryptocurrency community to seek more sustainable energy sources and technologies, which can improve the ESG scores of these digital assets.

Potential for Blockchain to Support Sustainability: Beyond cryptocurrencies, blockchain technology offers substantial potential for supporting sustainability through increased efficiency and transparency in various sectors. For example, blockchain can enhance the traceability of supply chains in commodities, ensuring that products are ethically sourced and sustainably produced. Additionally, blockchain platforms are being developed to facilitate carbon credit trading and renewable energy exchange, which could further enhance the sustainability profile of this technology.

3.4 Sustainable Investment Styles

Sustainable investment strategies integrate environmental, social, and governance (ESG) criteria into investment decisions not only to avoid risks but also to engage in opportunities that contribute to a sustainable global economy. These strategies range from exclusionary screening to proactive investment in themes that support sustainable development. Each approach reflects a different method of incorporating ESG factors, but all aim to align investments with broader ethical and financial goals.

3.4.1 Exclusionary Screening

Exclusionary screening is the process of omitting sectors, companies, or practices from investment consideration based on specific ESG criteria. This approach, also known as negative screening, is one of the oldest and most straightforward sustainable investment strategies. It is often used by investors who wish to align their investments with their ethical values by avoiding industries that they believe have a negative impact on society or the environment.

Origins: The origins of exclusionary screening date back to the 1960s and 1970s, closely tied to the social movements of the time, including anti-war and civil rights activism. Initially, this approach focused primarily on avoiding investments in companies associated with the Vietnam War or apartheid in South Africa.

Evolution: Over the years, exclusionary screening expanded to include a broader range of issues such as tobacco, alcohol, firearms, and fossil fuels, especially as public awareness of health and social issues grew.

Common Exclusions:

- Tobacco: Companies involved in tobacco production are frequently excluded due to health concerns and the societal impact of smoking.

- Firearms: Excluded due to ethical concerns over gun violence and its societal repercussions.

- Fossil Fuels: Increasingly excluded by investors focused on climate change, due to the significant role fossil fuels play in carbon emissions and environmental degradation.

According to the 2020 Trends Report by the US SIF Foundation, more than $640 billion of professionally managed assets in the United States apply exclusionary screens, demonstrating the significant scale and impact of this approach.

3.4.2 Inclusionary Strategies

Inclusionary strategies, or positive screening, involve selecting companies or sectors for investment based on superior ESG performance relative to industry peers. This approach focuses on investing in leaders in sustainability, who are often presumed to be better positioned for long-term success due to their advanced risk management and innovative practices.

Investors utilize ESG ratings provided by agencies such as MSCI or Sustainalytics to identify and select companies that excel in managing ESG issues. These ratings help investors find companies with the best ESG practices in their respective industries.

Development: In the 1990s, as data availability improved and investors became more sophisticated, the focus shifted from merely excluding negatives to actively seeking out positive ESG performers. This shift marked the beginning of what we now call inclusionary strategies or positive screening.

The development of reliable ESG data and ratings facilitated this transition, allowing investors to identify leaders in sustainability across various industries.

3.4.3 Thematic Investing

Thematic investing focuses on specific ESG themes that are expected to yield financial returns and societal benefits. This approach often targets investments that contribute directly to sustainable development goals such as renewable energy, clean technology, and sustainable agriculture.

Emergence: Thematic investing emerged strongly in the early 2000s with a focus on specific themes such as renewable energy, water conservation, and green technology.

Adoption: This style gained momentum as governments around the world began to support sustainable development goals, driving capital towards projects and companies aligned with these themes.

Examples of Thematic Investments:

- Clean Energy: Investments in solar, wind, and other renewable energy sources.

- Sustainable Agriculture: Investing in organic farming operations or companies that produce agricultural technologies reducing environmental impact.

3.4.4 Impact Investing

Impact investing aims to generate specific beneficial social or environmental effects in addition to financial gains. This style is characterized by a commitment to measuring and reporting the social and environmental performance and progress of underlying investments. The term “impact investing” was coined in the mid-2000s, but the practice had been in place much earlier through private equity and venture capital investments focused on social impact.

Impact Measurement: Investors in this space often use frameworks like the Impact Reporting and Investment Standards (IRIS) or the Global Impact Investing Network (GIIN) to measure the outcomes of their investments.

The last decade has seen substantial growth in impact investing, with investors not only seeking financial returns but also looking to make a measurable social or environmental impact.

3.4.6 Integrated ESG Investing

Integrated ESG investing involves the inclusion of ESG factors into traditional financial analysis and investment decisions. This approach recognizes that ESG factors can identify material risks and growth opportunities and is increasingly seen as essential to prudent investing. While other styles have longer histories, integrated ESG investing has become prominent only in the last decade, as traditional investors have started to recognize that ESG factors are material to financial performance. Regarding its mainstream acceptance, integrated ESG Investing has quickly moved from a niche approach to a mainstream investment strategy, particularly as evidence mounts that integrating ESG factors can enhance risk-adjusted returns.

CFA Curriculum Connection: The CFA Institute includes ESG integration as part of its curriculum, recognizing the importance of ESG factors in comprehensive investment analysis. This approach is highlighted as enhancing traditional financial analysis by considering ESG risks and opportunities that can affect a company’s performance and valuation.

In IMAG several of these investment styles can be implemented. Stocks can be excluded based on their low ESG scores, or the industry they are traded in. Alternatively, the investment style could choose to only include those stocks that have above average ESG ratings. Alltogether, we encourage the players to adapt an integrated ESG approach, where financial performance is also taken into account.

3.5 Client Types and Sustainability Preferences

As sustainable investing matures, diverse investor groups are increasingly directing capital towards investments that align with their environmental, social, and governance (ESG) values. Understanding the motivations and preferences of these distinct investor types—retail investors, institutional investors, and high net worth individuals (HNWIs)—is crucial for financial professionals aiming to tailor sustainable investment solutions.

3.5.1 Retail Investors

Retail investors are individuals who commit their personal finances to investment products. Retail investors have increasingly expressed interest in aligning their investments with their personal values and beliefs, which often include environmental and social considerations. This shift is driven by a growing awareness of global issues such as climate change, social inequality, and corporate governance.

3.5.1.1 Motivations and Product Availability:

Individual Beliefs and Values: Many retail investors are motivated by the desire to contribute positively to the world while earning returns on their investments. They look for investment opportunities that promise not only financial gains but also a positive impact on society and the environment.

Increasing Availability of Sustainable Products: Financial institutions have responded to this demand by expanding the availability of sustainable investment products. These include mutual funds, ETFs, and green bonds that cater to varying levels of risk tolerance and investment horizons. For instance, Morningstar reported a 57% increase in sustainable fund offerings in 2020 alone.

3.5.2 Institutional Investors

Institutional investors such as pension funds, insurance companies, and university endowments manage large pools of capital and are influential in shaping market dynamics. Their approach to sustainability is often guided by fiduciary duties and a long-term investment horizon.

- Fiduciary Duty and Sustainability: Institutional investors are recognizing that ESG factors can significantly affect the financial performance and longevity of their investments. Incorporating sustainability is increasingly seen as part of their fiduciary duty to protect and grow the assets they manage.

- Market Influence: Due to their substantial financial influence, when these institutions commit to sustainable practices, they can drive broader market trends and encourage corporate ESG compliance by leveraging their investment capital.

Institutional Investors: A Major Force in ESG Investing

- Definition: Institutional investors include pension funds, insurance companies, and educational endowments. They manage large pools of capital and have significant influence over the markets.

- Magnitude of Influence: As of 2021, institutional investors globally manage approximately $85 trillion in assets, with a growing proportion directed towards ESG-focused investments.

- ESG Integration: A 2020 survey by the Global Sustainable Investment Alliance (GSIA) reported that sustainable investment strategies are now being applied to $35.3 trillion in assets, representing over a third of all professionally managed assets globally. Institutional investors play a crucial role in this movement.

- Driving Factors: Factors driving ESG integration include risk management, fiduciary duty, and potential for enhanced returns. Climate change and corporate governance are particularly significant concerns.

- Interesting Fact: According to CERES, over 60% of the 100 largest US pension funds have committed to various degrees of ESG integration in their investment processes, citing long-term value creation and risk mitigation as key drivers.

3.5.3 High Net Worth Individuals (HNWIs)

High net worth individuals often have more flexibility in their investment choices and a greater ability to influence outcomes. They can pursue more aggressive strategies for impact investing and are often interested in how their wealth can contribute to a lasting legacy of social and environmental good.

- Values Alignment and Legacy: Many HNWIs are focused on how their investments can reflect their personal ethics and contribute to lasting social and environmental impacts. They often pursue investments that promise to leave a positive legacy.

- Catalyzing Innovation: With the capacity to undertake higher-risk investments, HNWIs frequently invest in cutting-edge sustainable technologies and startups. Their capital can act as a crucial catalyst for innovative ventures that might struggle to find funding through traditional channels.

HNWIs: Pioneers of Impact and Thematic Investing

- Definition: High net worth individuals are defined as having investable assets of over $1 million, not including primary residence and consumables.

- Growing Interest in ESG: The Capgemini World Wealth Report 2021 notes that nearly 41% of HNWIs globally are inclined to place up to half of their funds into ESG investments, reflecting a significant shift towards sustainable investing.

- Impact Investing: HNWIs are increasingly engaging in impact investing, seeking not only financial returns but also to generate a measurable, beneficial social or environmental impact.

- Catalytic Capital: Many HNWIs use their wealth to fund innovative startups in sustainable technology, renewable energy, and social enterprises, often taking positions that traditional investors might deem too risky.

- Interesting Fact: The UBS Investor Watch Survey found that 39% of HNWIs believe that their investment can lead to climate change solutions, and nearly one-third have reviewed their portfolios for climate impact, indicating a proactive stance in sustainability.

The clients in IMAG might be adhereing to ESG demand (e.g. a conservative ESG investor such as … or a dynamic ESG investor, imagine a …). All our clients are relatively wealthy but come to your investment company as they expect that you have the best expertise in catering to their needs. But be aware: Competition is fierce and ESG investors want to have an impact combined with financial returns. They will be quickly transferring to another company, due to their better alignment with their investment goals!

3.5.4 Conclusion

The diversity of investor types enriches the landscape of sustainable investing, each bringing unique perspectives and motivations. Retail investors are expanding access to sustainable products, institutional investors are embedding ESG considerations into their core strategies, and HNWIs are pushing the boundaries of what sustainable investments can achieve. Together, these dynamics are pivotal in driving the growth and effectiveness of sustainable investing practices globally.