Are There Fences in the Global Factor Zoo?

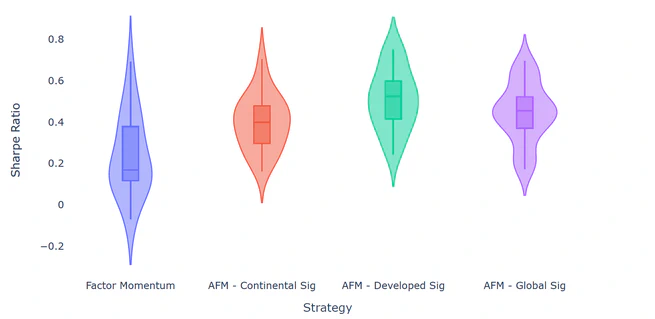

Regional and global factor momentum signals outperform local factors in forecasting risk premiums and revitalize momentum investing in less-integrated markets like Japan.

Habilitation, 2024

University of Liechtenstein

PhD Economics, 2015

University of Innsbruck

MSc Business Admin., 2007

University of Innsbruck

MSc Techn. Mathematics, 2007

University of Innsbruck

| Logo | Description |

|---|---|

my crypto2-package to retrieve

survivorship bias free cryptocurrency data from

coinmarketcap.com | |

my ffdownload-package to retrieve

research data from

Kenneth French's famous website | |

my rqmoms-package to calculate

option-implied moments according to

Grigory Vilkovs's python package |

Regional and global factor momentum signals outperform local factors in forecasting risk premiums and revitalize momentum investing in less-integrated markets like Japan.

We document a cross-country factor momentum anomaly, which we term ‘Factor Chasing’. Specialized style mutual funds chase factor returns across countries, but their trades are delayed, leading to positive returns that are not spanned by leading factor models.

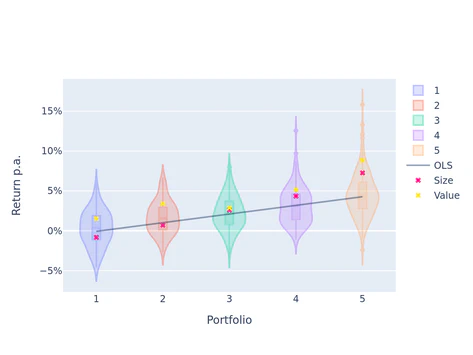

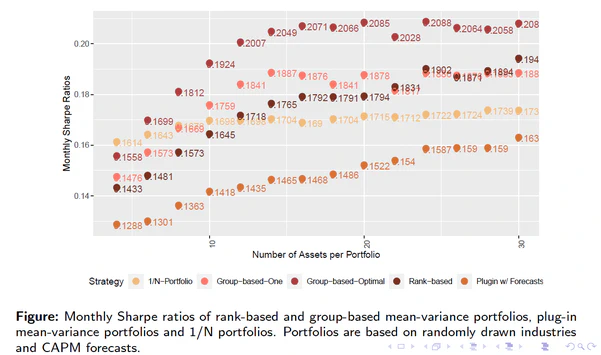

We offer a novel approach that aims at mitigating the crippling effects that parameter uncertainty and estimation errors have on the out-of-sample perforance of mean-variance optimized portfolios. We argue that investors should not rely on exact forecasts when optimizing portfolios but instead base their optimizations on ranking or grouping information and thereby implicitly reduce the informational content of their parameter inputs.

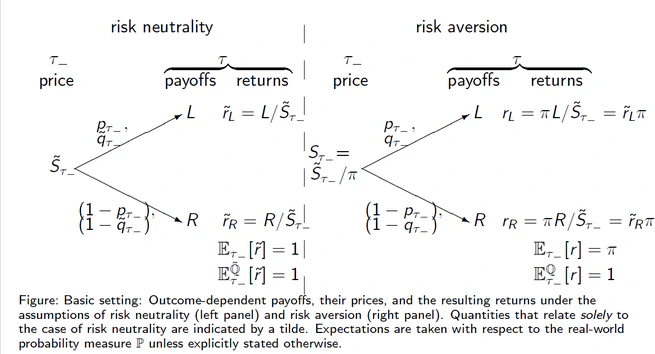

We analyze event risk premia in an expected utility framework and provide closed-form solutions under both quadratic and power utility for four different cases: Deterministic/stochastic conditional event returns, and deterministic/stochastic event outcome probabilities.

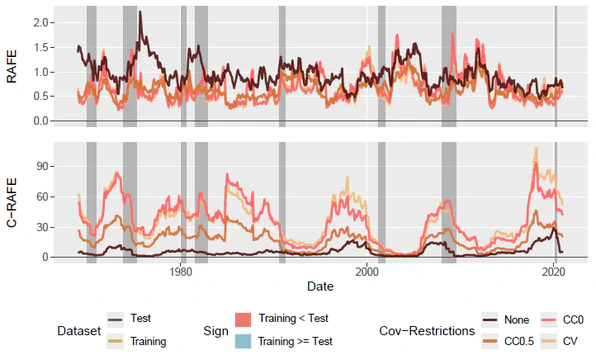

This paper proposes a multivariate risk-adjusted error measure for economic forecast performance and analyzes the limitations of traditional MSE-based measures in capturing the economic value of return forecasts.

We examine the effect of populism on financial markets around national elections. We find that the electoral success of populist parties has a direct impact on volatility in major domestic market indexes with different signs depending on the political ideology of the populist parties.

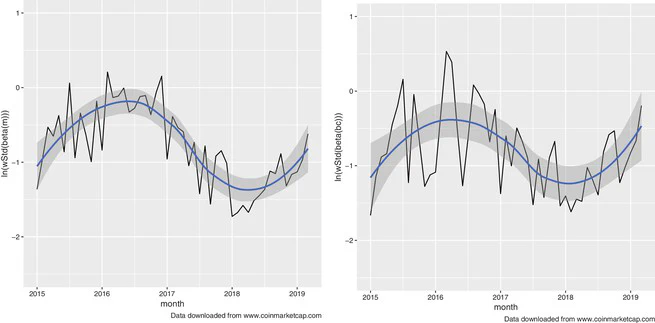

This paper investigates herding behavior in the crypto market. We consider the full, survivorship-bias free cross-section of cryptocurrencies, and document - against existing evidence - significant herding in this dataset. The effect is stronger, when using bitcoin as a transfer currency.

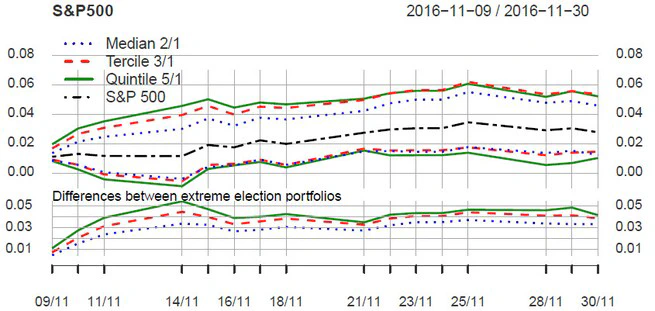

We use data from betting markets to analyze the sensitivity of stock returns to potential outcomes of political events such as elections. By classifying stocks into expected conditional winners and losers prior to such an event, we form portfolios that generate large positive returns after the event date, conditional on correctly anticipating the outcome. We illustrate this using data from the 2016 US presidential election and the 2016 Brexit referendum.

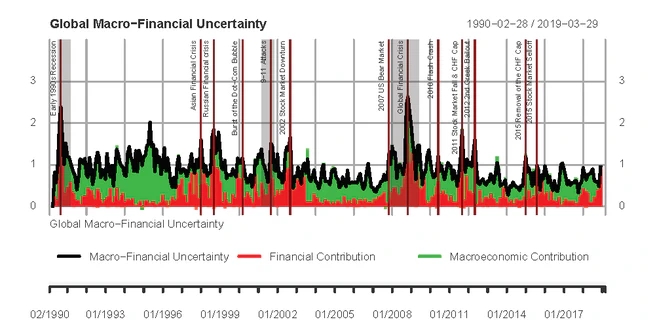

This paper introduces a novel measure of global macro-financial uncertainty and examines the state-dependent transmission of uncertainty to economic activity.

Bias-corrected asset pricing, market structure, and banking contagion in cryptocurrency markets — plus the open-source data infrastructure that makes the work possible.

Methods for selecting, timing, and combining factors when the zoo is crowded, the cross-section is noisy, and estimation error dominates.

Using market prices to measure how political events and populist electoral shifts are priced into equities, volatility, and cross-country asset returns.

Closing the gap between statistical forecast accuracy and the Sharpe ratio investors actually care about.

Measuring, pricing, and hedging the fact that investors do not know the true distribution of returns.

Erasmus+ project (2022–2025) delivering digital finance education through an online investment simulation — the Cesim Invest platform — for schools, universities, and professional training across Europe.

Developed an R-package and public Shiny app to optimize pension decisions for individuals in Liechtenstein's pension system, using large-scale optimization and machine learning.

Erasmus+ project (2019–2022) developing free online courses and interactive tools for life-cycle investments and personal financial planning — for the general public and higher-education students across Europe.

Erasmus+ project (2016–2019) developing free online courses and interactive tools for pension finance and personal pension planning — for the general public and higher-education students across Europe.

Reach out via email or directly book an appointment.

Fürst-Franz-Josef-Strasse

Vaduz, 9490

Liechtenstein

Monday 11:00 to 12:00

Otherwise book an appointment