Risk-Adjusted Forecast Performance

Closing the gap between statistical forecast accuracy and the Sharpe ratio investors actually care about.

•

2 min read

Closing the gap between statistical forecast accuracy and the Sharpe ratio investors actually care about.

Methods for selecting, timing, and combining factors when the zoo is crowded, the cross-section is noisy, and estimation error dominates.

This paper decomposes the Sharpe-ratio gap — the performance cost of estimation error in mean-variance investing — into a mean-forecast error (RAFE) and a precision-alignment error …

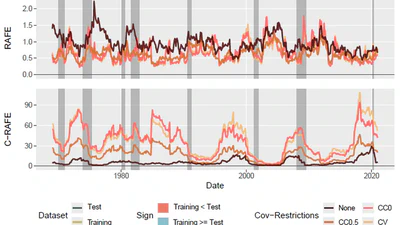

This paper proposes a multivariate risk-adjusted error measure for economic forecast performance and analyzes the limitations of traditional MSE-based measures in capturing the …

Unsupervised ML clustering of assets into equally weighted sub-portfolios dominates both plug-in minimum variance and equally weighted benchmarks, with optimal cluster count around …