Higher Moments Matter! Cross-Sectional (Higher) Moments and the Predictability of Stock Returns

In this paper we investigate the predictive power of cross-sectional volatility, skewness and kurtosis for future stock returns.

Sebastian Stöckl

In this paper we investigate the predictive power of cross-sectional volatility, skewness and kurtosis for future stock returns.

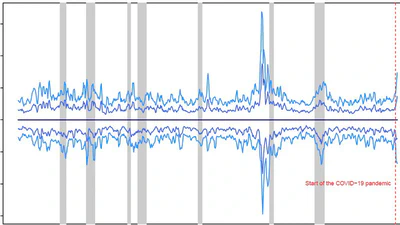

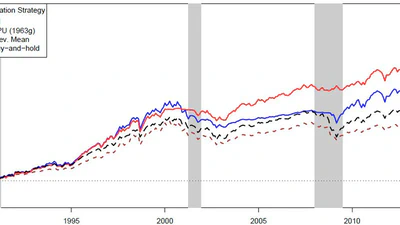

In this paper, we develop a novel, intuitive and objective measure of time-varying parameter uncertainty (PU) based on a simple statistical test.

Do forecasting errors from direct predictions of market components out-way the additional errors introduced by an intermediary asset pricing model?