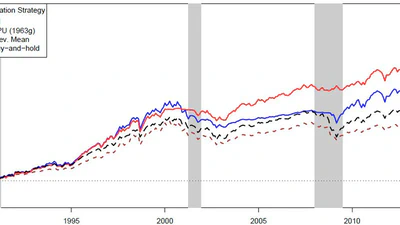

Parameter Uncertainty, Financial Turbulence and Aggregate Stock Returns

In this paper, we develop a novel, intuitive and objective measure of time-varying parameter uncertainty (PU) based on a simple statistical test.

Sebastian Stöckl

In this paper, we develop a novel, intuitive and objective measure of time-varying parameter uncertainty (PU) based on a simple statistical test.

We show that parameter uncertainty based on the turbulence within each cross-section of factor portfolios produces a significant out-of-sample forecast for six out of seven tested …

Based on a multidisciplinary literature review, we discuss the assumptions implicit in the prevalent Black-Scholes model and argue for relaxed assumptions that better represent …

Do forecasting errors from direct predictions of market components out-way the additional errors introduced by an intermediary asset pricing model?