Survivorship and Delisting Bias in Cryptocurrency Markets

Abstract

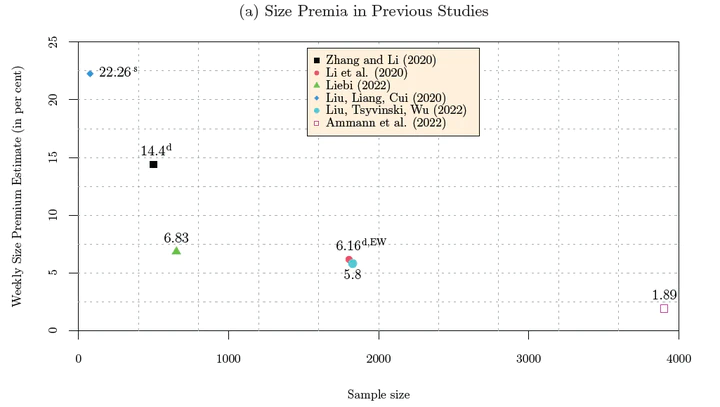

This study quantifies performance measures distortions in a cryptocurrency sample truncated by survivorship and delisting bias. Previous research shows that the attrition rate in cryptocurrency markets is high. However, the survivorship and delisting bias in cryptocurrencies lacks empirical research. Using data for 3’904 cryptocurrencies during the 2014-2021 period, we estimate an annualized survivorship bias of 0.93% (62.19%) for value-weighted (equal-weighted) portfolios. After controlling for survivorship and delisting bias, we revisit the relationship between average returns, size, past performance, and market beta. Our results confirm the size effect, but the premium is significantly inflated in a survival-conditioned sample. In contrast, we find no evidence of a positive relationship between average returns, momentum, and market beta. Our results suggest that besides the survivorship bias, the selection bias significantly affects the variation of results in previous studies.

Sebastian Stöckl

Assistant Professor in Financial Economics (tenure-track)

My research interests include Financial and Economic Uncertainty as well as Empirical Asset Pricing.