Regime-dependent drivers of the EUR/CHF exchange rate

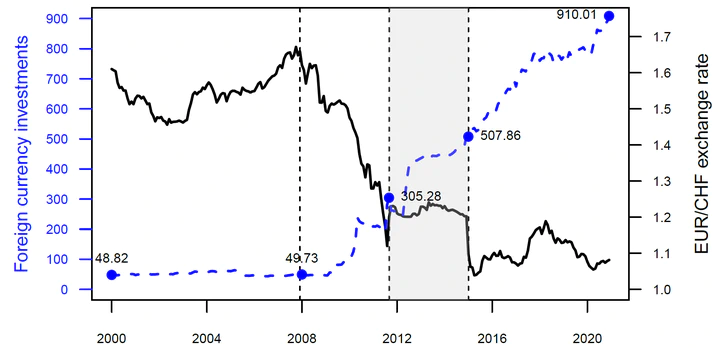

Development of the SNB’s foreign currency investments (FCI) in billion CHF (left vertical axis, blue dashed line) and the observed EUR/CHF exchange rate (right vertical axis, black solid line)

Development of the SNB’s foreign currency investments (FCI) in billion CHF (left vertical axis, blue dashed line) and the observed EUR/CHF exchange rate (right vertical axis, black solid line)Abstract

We analyze drivers of the EUR/CHF exchange rate in different regimes between 2000 and 2020. Structural breaks between these subperiods are estimated in an integrated way together with the drivers that are relevant during these subperiods. Overall, the main drivers of the exchange rate include European equity and volatility indices, interest rate and term structure slope differentials, as well as monetary policy interventions. For the ‘peg period’ Sept. 2011–Jan. 2015, in addition to the observed exchange rate we also analyze the drivers of the latent exchange rate that could have been observed in the absence of the peg. Interestingly, the SNB’s foreign currency investments became a significant driver of the EUR/CHF exchange rate only after the end of the peg period when there was no longer an officially communicated target rate.

Sebastian Stöckl

Assistant Professor in Financial Economics (tenure-track)

My research interests include Financial and Economic Uncertainty as well as Empirical Asset Pricing.