Parameter Uncertainty, Financial Turbulence and Aggregate Stock Returns

Abstract

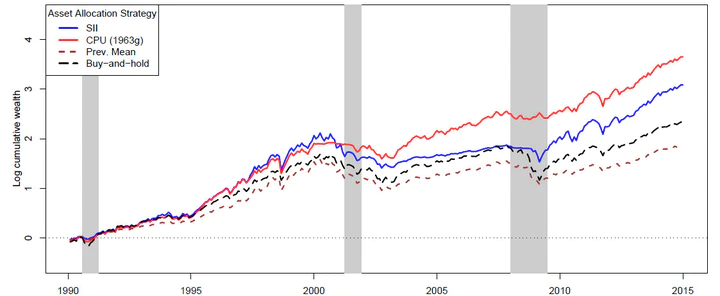

In this paper, we develop a novel, intuitive and objective measure of time-varying parameter uncertainty (PU) based on a simple statistical test. Investors who are averse to parameter uncertainty will react to elevated levels of PU by withdrawing from the market and causing prices to fall, a behavior that is well described by the model of portfolio selection with parameter uncertainty of Garlappi et al. (2007). We show that this model in combination with our measure, outperforms all other tested variables including the strongest known predictor to date. Additionally, it is the only predictor that fulfills all criteria generally expected from a stable predictor of the equity premium. All our results are statistically and economically significant and robust to a large variety of different specifications.

Sebastian Stöckl

Assistant Professor in Financial Economics (tenure-track)

My research interests include Financial and Economic Uncertainty as well as Empirical Asset Pricing.