Breaking Bad: Parameter Uncertainty Caused by Structural Breaks in Stocks

Abstract

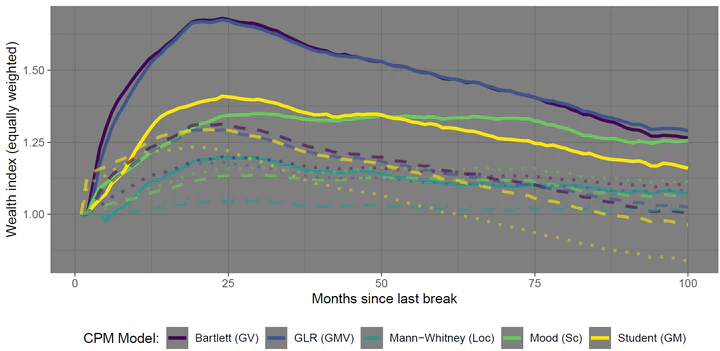

Estimating parameter inputs for portfolio optimization has been shown to be notoriously difficult and gets further complicated by structural breaks and regime shifts in financial data. We argue that these structural breaks ultimately result in parameter uncertainty, to which investors are averse. On an aggregate market level, this ambiguity-aversion gives rise to a premium for parameter uncertainty as stocks with high (low) parameter uncertainty are avoided/sold (more attractive/bought). We propose a novel measure called break-(adjusted stock-) age that proxies for parameter uncertainty and is based on detecting structural breaks in stock returns using unsupervised machine learning techniques. Our measure reveals (i) that break-age is priced significantly in the cross-section of stock returns and (ii) that break-age is a powerful proxy for parameter uncertainty.

Sebastian Stöckl

Assistant Professor in Financial Economics (tenure-track)

My research interests include Financial and Economic Uncertainty as well as Empirical Asset Pricing.